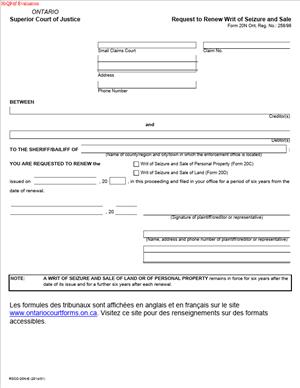

Form 20N – Request to Renew Writ of Seizure and Sale

Fill out nowJurisdiction: Country: Canada | Province or State: Ontario

What is a Form 20N – Request to Renew Writ of Seizure and Sale?

Form 20N is a Small Claims Court request to extend the life of a writ. A writ of seizure and sale lets the sheriff enforce your judgment. The writ authorizes seizure and sale of a debtor’s property. It can also bind the debtor’s land in a sheriff’s jurisdiction. A writ does not last forever. It expires after a set period if you do not renew it. Form 20N lets you renew before expiry. Renewal protects your enforcement rights for another term.

You use this form after you win a judgment and have a writ on file. It does not create a new judgment. It does not change your judgment. It keeps your existing writ active. That way, you can continue to enforce if needed.

The form is straightforward. You confirm the parties. You confirm the court file. You confirm the original writ details. You show the updated balance owing. You ask the court to renew the writ. When the clerk issues the renewed writ, you refile it with the sheriff. That keeps your registration active in the counties you choose.

Who typically uses this form?

Judgment creditors use this form. That includes individuals, landlords, trades, and small businesses. It also includes larger companies that sue in Small Claims Court. You may be self‑represented. You may have a lawyer or licensed paralegal. Collection agencies use it when they act for a creditor. Assignees of a judgment also use it once they are on record with the court.

Why would you need this form?

You need renewal to avoid a lapse. If your writ expires, you lose its protective effect. You may lose your place in line against other creditors. If you renew on time, your writ stays in force. That helps if the debtor sells property. It helps if new assets appear later. It helps if you are in a payment plan and need backup.

Renewal is also practical. Many debtors need time to pay. Payments may be slow or irregular. You may have a garnishment but still have a balance. Renewal preserves your ability to enforce when needed. It signals you still intend to collect.

Typical usage scenarios

You won a judgment two years ago and filed a writ. The debtor made small payments but stopped. A real estate agent tells you the debtor listed a house. You renew the writ to keep it binding on that land. You want the writ to show up when the property sells.

You are a landlord with a judgment for arrears. The tenant moved to another county. You filed the writ in the new county’s sheriff office. The six‑year mark approaches. You renew to keep both registrations active.

You are a contractor who recorded a writ after trial. The debtor runs a seasonal business. You plan to levy on equipment if needed. You renew to keep that option open. You also plan to search for other counties if the debtor expands.

You are a self‑employed consultant. The debtor opened a consumer proposal that later failed. The stay is gone. You keep your writ renewed so the sheriff can enforce when assets appear.

When Would You Use a Form 20N – Request to Renew Writ of Seizure and Sale?

You use Form 20N when your writ’s expiry date approaches. Do not wait until the last week. Court processing and sheriff filing take time. Aim to renew a few months before expiry. That gives you time to gather the balance, calculate interest, and file. It also gives time to re‑register with each sheriff’s office.

You use it when the debtor still owes money. Even if you are not actively enforcing, you renew. Circumstances change. Debtors change jobs. Debtors buy or sell property. A renewed writ keeps you ready. It keeps your priority position against the debtor’s real estate in that jurisdiction.

You use it when you have a payment plan in place. A payment plan can fail. Renewal costs less than restarting enforcement later. Keep the writ alive while payments continue. If the debtor finishes paying before expiry, you can request a withdrawal.

You use it when you see a chance of recovery later. The debtor may be young and asset‑light now. They could inherit property. They could buy a home. They could change careers. Renewal protects your judgment during that time.

Typical users include landlords, trades, doctors, dentists, retailers, wholesalers, and professional firms. It also includes lenders, equipment lessors, and suppliers with unpaid invoices. You may be an insurer with a subrogated claim. You may be an individual who sued for damages. If you hold a Small Claims Court judgment and already have a writ, this form applies.

You also use it if you filed the writ in more than one county. Writs bind land within the sheriff’s jurisdiction. If the debtor owns land in multiple counties, you file in each county. Renewal helps you keep all those filings current. You renew the writ through the court, then refile with each sheriff where it is registered.

Legal Characteristics of the Form 20N – Request to Renew Writ of Seizure and Sale

Form 20N is a procedural court form. When accepted and issued, it extends the life of your writ. It does not change the judgment. It does not change the terms of payment unless ordered. It preserves your right to enforce the judgment by sheriff. It also preserves the writ’s effect on land within the sheriff’s jurisdiction. That includes priority against the proceeds of a sale, subject to senior interests.

It is legally binding because it results in an issued court document. The Small Claims Court clerk issues the renewed writ under the court’s authority. The sheriff enforces only based on valid writs filed in that office. If your writ expires, the sheriff treats it as no longer active. Renewal ensures the sheriff can continue to act.

Enforceability depends on correct filing and accuracy. You must file Form 20N before the writ expires. You must state the outstanding amount honestly. You must account for payments received. You must apply postjudgment interest at the proper rate. The court can refuse or return forms that are incomplete or inaccurate. The sheriff can refuse to act if the filing is not current.

Several legal factors can affect enforcement. A stay of enforcement stops action on a writ. A stay can arise from an appeal, a bankruptcy, or a court order. A debtor’s bankruptcy can stay or release claims. Exemptions also limit what the sheriff can take. Basic household items are exempt up to set values. Tools of the trade are exempt up to set values. A vehicle may be exempt up to a limit. You can still keep a writ on file during these events. You cannot enforce while a stay exists. Renewal preserves your position for later.

Priority matters. Writ priority over land is tied to time of filing with the sheriff. If you let the writ lapse, you may lose that place in line. Later creditors could jump ahead on a sale. Renewal keeps continuity if you do it before expiry.

If a writ has already expired, the process is harder. You may need court permission to re‑issue enforcement. You may need a motion and an order. That takes time and cost. It may also affect priority. Renew on time to avoid that risk.

How to Fill Out a Form 20N – Request to Renew Writ of Seizure and Sale

You want a clean, accurate filing. Follow these steps. Keep copies of everything you file. Diarize future dates.

Step 1: Confirm your writ status and timeline

Find your original writ. Note the court file number and court location. Note the date the writ was issued. Note the sheriff’s enforcement office(s) where you filed it. Check your records for the expiry date. If you are unsure, contact the court to confirm the writ issue date. Give yourself at least 60 to 90 days to renew.

If the writ has already expired, pause. You likely need a different process. Consider seeking legal advice before you proceed. Do not file Form 20N if your writ has already lapsed without confirming next steps.

Step 2: Gather accurate balance information

You must state the current amount owing. Assemble your judgment, any cost awards, and the writ. Gather your payment history since judgment. Include dates and amounts. Note any costs added by later orders. Note any enforcement costs previously awarded.

Calculate post-judgment interest up to the date you will file. Use the postjudgment interest rate that applies to your judgment. If the judgment specifies a rate, use that rate. If not, use the rate set by law for post-judgment interest. Calculate simple interest on the unpaid principal, unless your order says otherwise.

Apply payments properly. Unless your order says otherwise, apply payments first to costs, then interest, then principal. Keep your math clear. If you are unsure of the interest rate or allocation, seek advice. Overstating a balance can cause problems with the court and sheriff.

Here is a simple example. Your judgment principal is $12,000. Costs awarded are $500. No prejudgment interest was awarded. The postjudgment interest rate is 3% per year. The debtor paid $2,000 a year after judgment. Two years have passed since judgment. Interest for the first year is $12,000 x 3% = $360. Apply the $2,000 payment first to costs ($500), then interest ($360), then principal ($1,140). The new principal is $10,860. Interest for the second year is $10,860 x 3% = $325.80. Your outstanding balance is $10,860 + $325.80 = $11,185.80. Use your actual dates for more precision.

Prepare a one‑page payment summary. It should show the starting amounts, each payment, interest calculation, and the resulting balance. You can attach this as a schedule if needed. Clear documentation reduces questions at the counter and with the sheriff.

Step 3: Complete the court and party details

Open the Form 20N. Fill in the court file number exactly as it appears on your case. Fill in the court location name. Use the same parties’ names as on the judgment. If a name has changed, ensure the court file reflects the change first. If the judgment was assigned, ensure the court has recorded the assignment. Use your current mailing address, phone, and email. The sheriff and court will need to reach you.

Enter the original writ issue date and writ file number if the form asks for it. If you filed the writ in multiple sheriff offices, list those enforcement offices. If you plan to add new counties now, note that renewal does not add new counties on its own. You will file the renewed writ with any additional sheriff offices after the court issues it.

Step 4: State the outstanding amounts

The form will ask for amounts. Separate principal, costs, interest, and credits received. Enter:

- Judgment principal still unpaid.

- Costs awarded and still unpaid.

- Postjudgment interest accrued to the filing date.

- Total payments received after judgment.

- The total balance now owing.

Keep the numbers consistent with your payment summary. Do not include enforcement costs that were not awarded by the court. If you have a later cost order, include that amount and cite the date. Do not include pre‑judgment interest unless it was awarded and remains unpaid.

Double‑check the interest period. Stop interest on the date you sign the form. If more time passes before filing, update the interest and re‑sign.

Step 5: Make the renewal request

The body of the form contains the request. It states you ask the court to renew the writ. It will refer to the original writ details. Read the request language. Confirm it matches your file.

Some forms include a statement of truth. By signing, you confirm the facts and amounts are true. Treat this as a sworn statement. Accuracy is critical. The court can refuse to act on forms that are wrong or misleading.

Step 6: Sign and date

Sign the form. Print your name and role. If you are a representative, include your firm name and contact details. Date the form. Make sure the date matches your interest calculation. If someone signs for a creditor company, ensure they have authority. If a paralegal or lawyer signs, they sign in their representative capacity.

Step 7: Attach any helpful schedules

Attach your payment and interest summary if space is tight. Attach any recent cost orders that affect the balance. Mark each attachment clearly. Reference it in the form if there is a section for attachments. Keep attachments concise and readable.

Step 8: File the form with the Small Claims Court

Make at least two copies. File the original with the Small Claims Court where the case is filed. Pay the filing fee. Ask for a stamped copy for your records. Confirm how you will receive the issued renewal. Some courts return it by pickup. Some send it by mail or email. Processing times vary. Build in time.

You do not usually need to serve the debtor with this request. Renewal is an administrative step with the court. If the court requires any further step, the clerk will advise you.

Step 9: Obtain the renewed writ and refile with the sheriff

When the court issues the renewed writ, review it for accuracy. Confirm the parties, file number, and amounts. Confirm the new expiry date. Make several certified copies if needed.

File the renewed writ with each sheriff’s enforcement office where you want it active. Include the sheriff’s fee, if any. If your original writ was filed in two counties, file in both again. If you want to add a new county, file the renewed writ there as well. Keep proof of filing and receipts.

Ask the sheriff to confirm registration details. Some offices provide a receipt with the writ number and date. Keep this with your enforcement file.

Step 10: Update your enforcement plan and diary

Note the new expiry date in your calendar. Set reminders at four years, five years, and six months before expiry. This helps you avoid a scramble later. Review the debtor’s situation yearly. Consider whether to search for new counties or assets. Consider whether to seek a garnishment if you learn of employment. Match your enforcement activity to the debtor’s situation.

Practical tips to avoid common mistakes

Use the correct interest rate. If your judgment states a rate, use that rate. If not, use the postjudgment rate for the relevant period. Do not compound interest unless the order allows it.

Do not overstate amounts. Include only amounts ordered and unpaid. If you incurred enforcement costs not yet awarded, do not add them until an order allows it.

Keep names consistent. Use the exact legal names from the judgment. If a company has changed its name, update the court file first. If you bought the judgment, record the assignment with the court before you sign as creditor.

Mind stays of enforcement. If a stay exists, do not attempt enforcement. You can still renew the writ to preserve rights, but you must not act while the stay is in place.

File early. Clerk and sheriff timelines vary. Mailing adds delay. Build a buffer.

Real‑world examples of completion

A landlord won $6,800 plus $300 costs three years ago. No interest rate was specified. The postjudgment rate averaged 2% per year. The tenant paid $1,500 over two payments. The landlord calculates interest each year on the unpaid principal. Payments are applied to costs, then interest, then principal. The current balance totals $5,950. The landlord completes Form 20N with those figures. They file it two months before expiry. The court issues the renewal. The landlord files it with the sheriff in the county where the tenant now lives.

A contractor won $14,500 plus $800 costs five years ago. The judgment set 4% postjudgment interest. The debtor made no payments. The six‑year term is close. The contractor calculates five years of interest on the full principal. They confirm no payments to deduct. They file Form 20N and then refile the renewed writ in two counties. They also plan a levy on equipment at season’s end.

What happens after you renew

Renewal does not force the sheriff to act. You still need to give the sheriff instructions to enforce. For example, you might ask the sheriff to seize and sell non‑exempt assets. You might ask the sheriff to act when a sale proceeds. You may also use other enforcement tools like garnishment while the writ is active. Maintain contact with the sheriff as needed.

If the debtor pays the full balance after renewal, file a withdrawal of the writ. That clears the registration from the sheriff’s records. It is your duty to clear paid writs. Failing to do so can cause issues for the debtor and lead to court concerns.

Key takeaways before you start

Form 20N is about preservation. It keeps your writ alive and effective. It protects your priority and your leverage. It is simple but detail‑sensitive. Get the balance right. File early. Refile with each sheriff. Keep clean records. If you do these steps, you maintain a strong enforcement position for the next term.

Legal Terms You Might Encounter

Judgment: This is the court’s decision that you are owed money. The writ enforces this judgment. When you renew the writ, you are not changing the judgment. You are keeping your enforcement rights active.

Judgment creditor: That’s you, the person or business the court says is owed money. On this form, you confirm your information so the court can match the renewal to the right case and writ.

Judgment debtor: This is the person or business who owes you money under the judgment. Use the debtor’s exact legal name on the form. That helps the enforcement office find assets and avoid mismatches.

Writ of Seizure and Sale: This is an enforcement document that lets the enforcement office seize and sell the debtor’s property within the county or district. Renewal keeps the writ alive so it remains searchable and enforceable.

Enforcement office (Sheriff): This office enforces writs within a specific county or district. You file or maintain your writ there. The form asks you to identify each enforcement office where your writ is filed so renewal reaches the right places.

Writ number and court file number: The court assigns these numbers when the writ is issued. They are not the same. The court file number tracks the lawsuit. The writ number tracks the enforcement document. You include both so the clerk can renew the correct writ.

Expiry date: Writs are only valid for a set period. After that, they lapse unless renewed. Renewal prevents a lapse. If a writ lapses, you may lose enforcement rights or priority, and you may need extra steps to revive enforcement.

Renewal: Renewal extends the life of your writ for another period allowed by the rules. It does not create a new judgment. It keeps the existing writ active so you can continue enforcement.

Priority: Priority is the order in which creditors get paid from seized assets. A lapsed writ can lose its place in line. Renewing on time protects your position against other creditors.

Postjudgment interest: Interest that accrues after the judgment date. Renewal does not change the interest rate or calculation method. You still track interest as allowed, and you can update your records with the enforcement office.

Disbursements and costs: These are amounts you spend to enforce the judgment, like filing fees. You may add allowable amounts to your claim as the rules permit. Renewal does not automatically add costs; it preserves the writ so you can continue enforcement and recover eligible costs.

FAQs

Do you have to renew before the writ expires?

Yes. File the request before the writ’s expiry. If you wait, the writ can lapse, your enforcement can stop, and you may lose priority. Renewal before expiry is the simplest and fastest route.

Can you renew if the writ already expired?

It may be harder. A lapsed writ may require additional steps and court direction. You might need a different process rather than a simple renewal. Act early to avoid this problem.

How long does a renewed writ remain in force?

A renewed writ remains in effect for another defined period under the rules. The renewed term begins when the renewal takes effect. Check your stamped renewal for the new expiry date and diary it well in advance.

Do you need the debtor’s consent or to give notice to renew?

You usually do not need the debtor’s consent to renew. Renewal is an administrative step to keep an existing writ active. If the court requires notice in a specific situation, the clerk will tell you.

Does renewing change the amount owed or the interest?

No. Renewal does not change the judgment or the interest rules. It keeps your enforcement rights alive. Interest continues to accrue as allowed. Update your running balance with credits, payments, and permitted costs.

What if the debtor moved or changed their legal name?

Renewal still applies to the same debtor. Use the correct current legal name if you know it, and keep prior names that appear on the original writ. If the debtor has moved, consider filing or maintaining the writ in each relevant enforcement office to reach assets in those areas.

Do you need to refile with every enforcement office after renewal?

Confirm what each enforcement office requires. Many offices expect a renewed copy or confirmation for their records. Failing to update an office can leave the writ inactive in that location.

What happens if the debtor pays you after you renew?

You can continue to enforce until paid in full. Once paid, you should take steps to withdraw or satisfy the writ so public records reflect the payment. Keep proof of payment and any withdrawal or satisfaction filing in your file.

Checklist: Before, During, and After

Before signing: Information and documents you need

- Court file number from your Small Claims Court case.

- Writ number and the original writ issue date.

- Exact legal names of the judgment creditor(s) and debtor(s).

- Current contact details for you or your representative.

- The enforcement office(s) where the writ is filed, by county or district.

- The outstanding balance as of a chosen date, with your interest calculation.

- Records of credits and payments received since the writ issued.

- Any prior renewals and the current writ expiry date.

- Documents showing name changes for the debtor or creditor, if any.

- Method of payment for filing fees.

- Access to your original judgment and any amending orders, if applicable.

During signing: Sections to verify carefully

- Names: Match the court file, judgment, and original writ. Watch spelling and order.

- Numbers: Court file number and writ number must be accurate and legible.

- Writ details: Confirm the original issue date and the enforcement office locations.

- Amount: Ensure the balance reflects credits and interest as allowed.

- Tick boxes or selections: If the form distinguishes land or personal property, select correctly.

- Dates: Insert the date you sign. Avoid backdating or leaving dates blank.

- Signature: Sign where required. If an agent signs, include their title and authority.

- Attachments: If the form allows schedules for multiple offices or parties, include them.

- Legibility: Print neatly if completing by hand. Illegible forms can be rejected.

After signing: Filing, notifying, and storing

- File the form with the Small Claims Court that issued the writ. Pay the fee.

- Ask for a stamped copy or written confirmation of renewal for your records.

- Obtain copies to provide to each enforcement office where the writ is registered.

- Deliver or file the renewed writ with each enforcement office as required.

- Confirm that each office shows the new expiry date in its index.

- Update your internal ledger for balance, interest date, and costs.

- Calendar the new expiry date with reminders 6–12 months in advance.

- Note any follow-up steps, such as scheduled asset searches or examinations.

- Store the stamped renewal, proof of filing, and delivery receipts in your file.

- If you use an agent or collector, send them the renewed writ and instructions.

Common Mistakes to Avoid

Waiting until the last minute. Don’t forget that a writ lapses on expiry. If it lapses, you may lose priority and face extra steps to revive enforcement. File early so the clerk can process your request before the deadline.

Using the wrong legal name for the debtor. Don’t rely on nicknames or short forms. If the name is wrong, the enforcement office may not match assets. Use the name on the judgment and include aliases that appear on your court record.

Mixing up the court file number and writ number. Don’t transpose digits or swap them. The clerk needs both numbers to renew the correct writ. Double-check against your original writ and court documents.

Not updating enforcement offices. Don’t assume renewal at court updates every office automatically. Some offices need updated copies or confirmations. Failure to update can leave your writ inactive in that location.

Incorrect balance or interest date. Don’t overstate or omit credits. An inaccurate balance can cause disputes or delay enforcement. Keep a clear interest calculation to your chosen date, and keep backup records.

What to Do After Filling Out the Form

- File the request. Take the signed form to the Small Claims Court that issued the writ. Pay the filing fee. Ask for a stamped copy or written confirmation. If the clerk needs corrections, fix them promptly and refile.

- Track the renewal decision. Check for acceptance. If the court rejects the request, ask what to fix. If accepted, note the new expiry date and place it on your calendar with early reminders.

- Update enforcement offices. Send each enforcement office a copy of the renewed writ or renewal confirmation as they require. Ask them to confirm the new expiry date on their index. Keep delivery receipts and any responses.

- Align your enforcement plan. With the writ renewed, decide next steps: search for assets, schedule examinations, or maintain existing enforcement. Note any seasonal asset opportunities, such as tax refunds or property listings.

- Maintain accurate balances. Post any payments, add permitted costs, and update interest as allowed. Keep a simple ledger that shows principal, interest, credits, and disbursements. This helps you answer debtor inquiries and satisfy the writ later.

- Handle partial or full payment. If you receive full payment, prepare to withdraw or satisfy the writ. If partial, keep enforcing for the balance. Keep written proof of any payment agreements or plans.

- Address changes or errors. If you discover a name error or need to add an alias, follow the court process to amend or clarify the writ record. Keep consistent information across the judgment, writ, and enforcement office filings.

- Consider multiple locations. If the debtor has assets in more than one county or district, ensure the writ is maintained in each relevant enforcement office. Renewal alone at court may not reach new locations.

- Prepare for the next cycle. Set reminders for asset searches and follow-ups well before the next expiry window. Early action keeps you ahead of deadlines and protects your priority.

- Store everything. Keep the stamped renewal, proofs of filing, fee receipts, correspondence with enforcement offices, and your updated ledger. Save both digital and paper copies. A complete file speeds future renewals and satisfies audit requests.

Disclaimer: This guide is provided for informational purposes only and is not intended as legal advice. You should consult a legal professional.