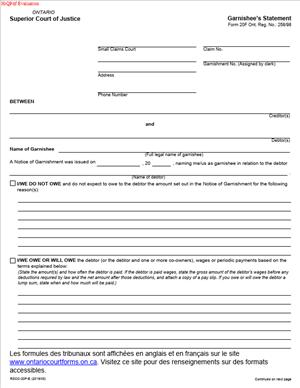

Form 20F – Garnishee’s Statement

Fill out nowJurisdiction: Country: Canada | Province or State: Ontario

What is a Form 20F – Garnishee’s Statement?

Form 20F is the Small Claims Court document a garnishee completes and files after being served with a Notice of Garnishment. In simple terms, if you owe money to a judgment debtor—now or in the future—the court requires you to confirm that debt and start paying the court instead of the debtor, up to the judgment amount. Form 20F tells the court what you owe, how and when you owe it, and how you will comply.

If you are an employer, bank, property manager, or business that pays the debtor, you are the garnishee. You did not choose to be involved in the lawsuit, but you now have court-ordered duties because money you hold or owe can be used to satisfy the debtor’s judgment.

Who typically uses this form?

Employers (payroll or HR), financial institutions (branches or head office teams), companies that owe the debtor on invoices or commissions, property managers who collect rent payable to the debtor, and payment processors who make scheduled payouts. In each case, you are paying or holding funds for the debtor.

You would need this form because you received a Notice of Garnishment naming you as garnishee. The law requires you to respond promptly, usually within 10 days of service. Form 20F is how you respond. If you do nothing, the court can order you—not the debtor—to pay, up to the amount that should have been withheld. Filing Form 20F protects you, clarifies your obligations, and avoids penalties.

Typical usage scenarios include:

- An employer who must deduct a portion of an employee’s net wages each pay and send it to the court.

- A bank that must hold and remit funds from the debtor’s account up to the garnishment amount.

- A customer that owes the debtor on an outstanding invoice and must pay the court rather than the debtor.

- A landlord who owes a rent refund or deposit to the debtor.

- A platform or broker that pays periodic commissions to the debtor.

In short, Form 20F is your official statement to the court about what you owe the debtor and how you will comply with the garnishment.

When Would You Use a Form 20F – Garnishee’s Statement?

You use Form 20F after you are served with a Notice of Garnishment naming your business or institution as a garnishee. It applies when you owe, hold, or will owe money to the debtor. You do not file Form 20F on your own initiative; it is triggered by service.

Consider practical examples:

You are an employer. Your payroll department receives a Notice of Garnishment for an employee. You must calculate the allowable deduction from each pay based on net wages. You file Form 20F within 10 days, confirm employment, set out the pay cycle and net amount, disclose any prior garnishments or support deductions, and state what you will deduct and remit to the court each pay.

You are a bank branch. You receive a Notice of Garnishment for a customer. You confirm whether the customer has accounts and what funds were available when you were served. You complete Form 20F, disclose the accounts, and remit available funds up to the amount stated. If there are no funds or no account, you state that.

You are a small business that owes the debtor on an invoice. The work is complete, and payment is due next week. You file Form 20F, confirm the amount due and payment date, and pay the court instead of the debtor when due.

You are a property manager who holds a rent deposit that is being returned. You file Form 20F and send the deposit to the court as required.

You are a marketplace that pays monthly commissions. You identify the periodic payout amount and dates, file Form 20F, and redirect the commissions to the court while the Notice of Garnishment remains in force.

You also use Form 20F to dispute or clarify liability. If you do not owe the debtor, if employment ended before service, if no account exists, or if you have a lawful set-off that reduces what you owe, you state that in the form with details and supporting facts.

In all of these situations, the Notice of Garnishment binds you to act. Form 20F records your response and guides how the court will manage the garnishment.

Legal Characteristics of the Form 20F – Garnishee’s Statement

Form 20F is part of a court-ordered enforcement process. It is not the order itself—the Notice of Garnishment is—but it is a required response with legal consequences. When you sign and file Form 20F, you are making an official statement to the court about your obligations. You must be accurate and complete. False or incomplete information can expose you to liability, costs, and court sanctions.

Is it legally binding? The enforcement comes from the Notice of Garnishment, which compels you to pay the court rather than the debtor, within defined limits. Your Form 20F confirms whether and how that obligation applies to you. Once served, you must comply. The court can hold a garnishee responsible for amounts that should have been paid if the garnishee ignores the notice or fails to respond. In short, the Notice binds, and the Form 20F documents compliance.

What ensures enforceability? Proper service of the Notice of Garnishment, a valid underlying judgment, and compliance with court rules. The court clerk issues the Notice for a specific amount. The notice typically remains in force until the judgment amount is paid, the notice expires, or the court terminates it. For periodic debts like wages, it continues to bind future payments. For non-periodic debts like bank account balances, it binds what was owed when served.

There are legal limits and priorities:

- Wages. Only a portion of net wages can be garnished for ordinary debts. Net wages mean after mandatory statutory deductions. You cannot calculate on gross pay. Do not withhold more than allowed. If court-ordered support deductions are in place, they have priority and may reduce or eliminate amounts available for other garnishments. Disclose existing deductions in Form 20F so the court can assess availability.

- Other debts. Money you owe the debtor under a contract, invoice, commission, or rent refund is generally garnishable up to the judgment amount. Those payments are not limited by wage-specific percentages, but timing matters—only debts due or accruing due when served are caught, unless they are periodic.

- Financial accounts. Funds in accounts held for the debtor are subject to garnishment up to the available balance when served. If there is less than the claimed amount, you remit what exists. If there are no funds or no account, you state that.

- Exemptions. Certain sources of income may be exempt from garnishment or subject to special rules. If you know you pay the debtor from a source that is exempt, note it clearly in Form 20F and do not withhold from exempt amounts. If you are unsure, disclose the facts and seek direction from the court if needed.

- Set‑off. If you had a legal right to set off amounts the debtor owed you that arose before service, you may be able to deduct those amounts from what you owe. You cannot create a set-off after service to defeat the garnishment. Disclose any set-off claim with details in the form.

- Sequence and priority among garnishments. Earlier garnishments and support deductions can impact how much you must withhold. Disclose all existing deductions in Form 20F.

Administrative fees. A garnishee making wage deductions may deduct a modest administrative fee from the employee’s pay for each remittance, as permitted by court rules. Do not add fees that are not allowed. Note any such deduction in your calculation.

Privacy and confidentiality. Form 20F goes to the court and the creditor. Include only the information the form asks for. Do not include a social insurance number or other sensitive identifiers unless required by the form. Use employee initials or a payroll ID if the form allows.

Bottom line: Form 20F is your official, timely, and accurate disclosure. The court uses it to manage enforcement and ensure legal limits are respected. Non-compliance can make you liable for amounts you should have paid.

How to Fill Out a Form 20F – Garnishee’s Statement

Follow these steps to complete and file the form correctly. Keep your sentences short and your records organized. Respond within 10 days of being served unless the notice states a different deadline.

1) Gather the documents and facts.

- Read the Notice of Garnishment carefully. Note the court file number, court location, debtor name, creditor name, and total amount claimed, including costs.

- Confirm the date and method of service on you. Your deadline runs from the service date.

- Identify what you owe the debtor: wages, bank funds, commission, invoice, rent, or nothing.

- Pull supporting records: payroll register, pay frequency, net pay calculation, account balances, invoices, contracts, and payment schedules.

2) Complete the court and party details.

- Enter the court file number from the Notice.

- Confirm the court location (the Small Claims Court office listed).

- Fill in the creditor’s and debtor’s names exactly as shown on the Notice.

- Insert your legal name as garnishee, your mailing address, phone, and email. If you operate under a trade name, include the legal entity name.

3) State whether you owe money to the debtor.

- If you owe nothing, check or state “not indebted” and explain why. Examples: no account exists, employment ended before service, invoice not approved and no contractual debt, or funds belong to a different person or entity. Be specific.

- If you owe money now or in the future, describe the type of debt and the timing.

4) If you are an employer, complete the wage section.

- Confirm employment status and date of hire. If employment ended, give the last day worked.

- State the pay frequency (weekly, bi-weekly, semi-monthly, monthly) and regular pay date.

- Calculate net wages per pay: gross earnings minus mandatory statutory deductions only. Do not subtract voluntary deductions or advances unless required by law or court order.

- Determine the maximum deduction allowed for ordinary debts. Calculate the percentage on net wages, not gross.

- Disclose all existing deductions that affect availability, such as support deductions or earlier garnishments. Include their amounts per pay.

- Provide the next pay date and the expected deduction amount for that pay. If the available amount is reduced to zero due to priority deductions, state that and explain.

- Note any allowed administrative fee you will deduct per remittance.

- Commit to remitting on each pay date while the notice is in force. If pay fluctuates, explain how you will recalculate each period.

Example: “Employee paid bi-weekly. Gross $1,200. Statutory deductions $300. Net $900. Maximum ordinary deduction calculated on net. Support deduction of $450 per pay in priority. No amount available for this garnishment until support ends or changes.”

5) If you are a bank or financial institution, complete the account section.

- Identify the customer (debtor) and the branch or unit that holds the account.

- State the account type and the balance available when you were served. If multiple accounts exist, list each with the available balance.

- If the balance is less than the amount claimed, you remit the available amount. If the balance is zero or the account is closed, state that.

- If funds are held on a joint account or are subject to restrictions, state the facts. Do not guess at ownership; describe what your records show.

- Note the date you will remit funds to the court and the amount.

6) If you owe the debtor on invoices, commissions, rent refunds, or other payments, complete the “other debts” section.

- Describe the contract or obligation. Example: “Invoice 1234 for completed services; due in 14 days.”

- State the amount due now and the due date. If the obligation is periodic (monthly commissions), provide the cycle, average amount, and next payment date.

- If you have a bona fide pre-existing set-off (for example, the debtor owes you for returned goods or a credit issued before service), state the amount and attach a short explanation with dates.

- Confirm that you will remit any amounts due to the court on the due date(s).

7) Address exemptions or special income sources.

- If you know the payment source is exempt from garnishment, say so and explain the source. Do not withhold from exempt funds.

- If you are unsure, disclose the facts and withhold only amounts you are certain are garnishable. Ask the court for direction if needed.

8) Provide payment and remittance details.

- Identify the Small Claims Court office on the Notice. You must send payments to the court, not to the creditor.

- State how often you will remit (each pay date, upon invoice due date, or as funds become available).

- Include the court file number and debtor name with every payment so the court credits it correctly.

- Keep proof of each remittance: date, amount, and method.

9) Sign and date the form.

- The form should be signed by someone with authority and knowledge of the records, such as a payroll manager, branch manager, or finance officer.

- Print your name and title. Date the form.

- By signing, you confirm the information is true to the best of your knowledge.

10) Serve and file the form.

- File Form 20F with the Small Claims Court office named on the Notice within 10 days of service.

- Deliver a copy to the creditor at the address on the Notice.

- Keep a copy for your records with proof of delivery.

11) Start remitting and keep records.

- Begin withholding and remitting on the next scheduled payment to the debtor that falls after service, within legal limits.

- Continue until you receive a court notice to stop, the total is paid, the notice expires, the debtor’s entitlement ends, or employment ends.

- If employment ends or the debt is fully paid, inform the court and the creditor in writing.

12) Update or correct as needed.

- If your initial information changes (for example, pay changes, new priority deductions arise, or funds become available), file an updated statement or a short letter to the court with the file number, and send a copy to the creditor.

- If you discover an error, correct it promptly and make any shortfall remittance without delay.

13) Common issues and how to handle them.

- Multiple garnishments. Apply legal priorities. Deduct for higher‑priority items first. If nothing remains for this garnishment, say so in your form and remit zero for that pay.

- Over‑deduction. If you withheld more than allowed, stop further withholding and contact the court for instructions. Do not refund the debtor directly without direction.

- No ongoing obligation. If you do not owe the debtor now and will not owe in the future, state that clearly with reasons. Example: “Independent contractor engagement ended before service; no amounts outstanding.”

- Set‑off claims. Only apply set‑off that existed before service. Document dates and amounts. Do not net out disputed or future claims.

14) Practical tips to get it right.

- Calculate on net wages only for wage garnishments.

- Never pay the creditor directly unless the court instructs you. Pay the court office on the Notice.

- Put the court file number on every payment.

- Include only the information requested. Do not include sensitive identifiers unless the form requires them.

- Assign a single point of contact in your organization for all communications on this file.

Real-world examples:

Employer example: You run a 15‑person construction company. You receive a Notice for your site supervisor. You calculate net pay at $1,100 bi‑weekly. You identify priority deductions that reduce availability. You file Form 20F in five days, state the numbers, and confirm you will remit on each pay date. You continue until the court confirms the amount is paid.

Bank example: Your branch is served regarding a customer. The account balance at service is $2,450. The Notice claims $5,000. You complete Form 20F, confirm the balance, and remit $2,450 to the court. You note no other accounts and sign. No further remittances are required unless another account becomes due.

Accounts payable example: You owe the debtor $3,000 in 10 days for delivered goods. You file Form 20F, disclose the upcoming payment, and send $3,000 to the court on the due date. You maintain proof of remittance and close out your obligation.

By answering accurately and on time, you comply with the court’s order, avoid liability, and keep the process efficient.

Legal Terms You Might Encounter

Garnishment is a court-backed process. It directs someone who owes the debtor money to pay the court instead. This form records your position in that process. It tells the court what you owe the debtor now or over time.

A garnishee is you. You are the person or business that may owe money to the debtor. You could be an employer, a bank, or a client. On this form, you confirm if you owe the debtor and how much.

A creditor is the person or business who won a judgment. They started the garnishment to collect what the court says is owed. You will see the creditor’s name on the notice you received and on this form.

A debtor is the person or business who owes money under a judgment. The form asks you to identify the debtor and your financial relationship with them. You explain what you owe the debtor, if anything.

A Notice of Garnishment is the court document you received. It orders you to hold and pay certain funds to the court. This form is your formal response to that notice. Read the notice for the time period and payment directions.

Net amount owing is the money you actually owe the debtor after legitimate deductions. For wages, you consider deductions listed in the notice. For accounts, you consider the current balance and any right of set‑off.

A continuing garnishment covers money that becomes payable over time. The most common example is wages. You report the pay cycle and expected amounts on this form. You also note when payments will occur.

Set‑off means the debtor owes you money too. You may have the right to subtract that debt from what you owe them. The form asks you to disclose any set‑off and explain the amount. Provide documents if requested.

Exempt funds are amounts the law protects from garnishment. Some payments may be exempt in whole or in part. If you believe funds are exempt, say so on this form. Describe the funds and why you believe they are exempt.

Remittance means paying money as directed. Do not guess where to send funds. Follow the notice. The form helps confirm what you will pay and when. Keep proof of every payment you make.

Service is the formal delivery of documents. The notice you received was served on you. After completing your statement, you must deliver it as the notice instructs. Follow those delivery rules and keep proof.

FAQs

Do you have to complete the form if you owe nothing?

Yes. You must respond even if you owe $0. State clearly that you owe nothing. Explain why, using dates and facts. For example, note that employment ended or the account is closed. Attach a brief record if available.

Do you use gross or net amounts for wages?

Use the approach set out in the notice. It generally requires net amounts after listed deductions. List your pay cycle and net pay. Show your calculation in simple steps. Keep the payroll records you used.

Do you pay the creditor directly?

No. Follow the payment instructions in the notice. Garnishments usually require payment to the court office. Do not pay the creditor unless the notice or a court direction says so. Keep receipts for every payment.

Do you include bonuses, commissions, or vacation pay?

Include amounts that become payable during the garnishment period. Note the type of payment and its date. If the amount varies, provide your best estimate and explain the method. Update the court if the figure changes later.

Do you still need to respond if the debtor left your employment?

Yes. You must still file the statement. State the last day worked and final pay date. Indicate any final amounts payable, such as accrued vacation. If nothing remains payable, say so clearly and state $0.

Do you handle multiple garnishments at once?

Yes. List any other orders affecting the same debtor and pay cycle. Explain how they affect the amount available. Follow the instructions in the notices for priority and payment routing. If unsure, ask the court office to confirm process steps.

Do joint bank accounts fall under a garnishment?

You still need to respond. State the type of account and the debtor’s interest you hold. Identify it as a joint account. Do not decide entitlement yourself. The court will determine how much, if any, is subject to payment.

Can you correct your statement after you file it?

Yes. If you made an error, prepare an updated statement. File it promptly. Send copies as the notice requires. Add a short cover note explaining the correction and the reason. Correct future payments as needed.

Do you have to respond by a deadline?

Yes. The notice sets a deadline for your statement and any first payment. Act quickly. If you cannot meet the deadline, contact the court office about process steps. Document all attempts to comply and any delays.

Checklist: Before, During, and After

Before signing:

- Read the Notice of Garnishment from start to finish.

- Verify the court file number, creditor, and debtor names.

- Confirm you are the correct garnishee.

- Identify your relationship with the debtor: employer, bank, or other.

- Gather payroll details: pay cycle, next pay date, net pay, and deductions.

- Gather account details: account types, balances, and interest timing.

- Check for any set‑off you can claim and the supporting contract.

- Check for any other orders or garnishments against the debtor.

- Review whether any funds may be exempt. Note the reasons.

- Confirm the payment routing and the deadline in the notice.

- Identify the authorized signer and their title.

- Prepare supporting records you may need to show on request.

During signing:

- Confirm the court file number matches the notice.

- Confirm the debtor’s full name and any identifier you use.

- State clearly whether you owe money to the debtor.

- If wages apply, state the pay cycle and net amounts.

- If accounts apply, state the current amount owing to the debtor.

- Describe any set‑off in plain terms and show the amount.

- Note any other orders affecting the same funds.

- If funds are exempt, describe them and why you believe so.

- Enter dates accurately for employment, payments, and account changes.

- Use real numbers, not rough guesses, unless clearly labeled as estimates.

- Sign and date the form. Print your name and role.

- Review every section for completeness and consistency.

After signing:

- File the statement as the notice instructs. Do it before the deadline.

- Send any required copies to the listed parties. Keep proof of delivery.

- Diary the next pay date or payment date. Note the amounts to remit.

- Remit payments exactly as directed. Use the file number on payments.

- Keep proof of each remittance and the calculation behind it.

- Monitor for changes: employment status, account status, or new orders.

- If something changes, file an updated statement promptly.

- Store all records securely for the required retention period.

- Close your file when the notice expires or the court confirms completion.

Common Mistakes to Avoid

Don’t ignore the deadline. Late statements or payments can lead to consequences. The court may make an order against you for the unpaid amount. Act the day you receive the notice.

Don’t use gross pay for wage calculations. Overstating net amounts can over‑withhold from the debtor. Understating can expose you to liability. Follow the notice and keep your math clear.

Don’t pay the creditor directly. Most garnishments require payment to the court. Paying the wrong party can leave you still liable. Follow the payment instructions exactly.

Don’t forget to disclose set‑off or other orders. If you hold a valid set‑off, state it. If other orders exist, list them. Omissions can cause double payment or non‑compliance.

Don’t skip updates when facts change. Job status, pay amounts, or account balances may change. File an updated statement and adjust remittances. Silence can create risk for you.

What to Do After Filling Out the Form

File the statement by the deadline. Use the filing method in the notice. Include the court file number on every page and any cover sheet. Keep a stamped or acknowledged copy for your records.

Deliver any required copies. The notice will list who must get a copy and how. Common recipients include the creditor and the debtor. Use a delivery method that gives you proof. Keep that proof with your file.

Set up payment workflows. For wages, coordinate with payroll. Flag the file number and remittance method. For accounts, place a hold consistent with the notice. Schedule payments for the stated dates.

Remit as instructed. Use the exact payee and address. Include the court file number on the payment. Match each remittance to a calculation sheet. Save confirmations and receipts.

Track balances and timing. Note how much the notice seeks and what you have paid. Stop remitting when the notice expires or the court directs. If the debtor’s earnings vary, adjust each cycle and document why.

Handle changes promptly. If the debtor leaves employment, file an update. If the account closes, report the date and final balance. If you discover exempt funds, say so and hold as the notice allows.

Correct errors quickly. Prepare an updated statement if you find a mistake. File it and send required copies. Adjust future remittances to fix the error. Keep a short note explaining what changed and when.

Close out properly. When you reach the total amount or the notice ends, stop payments. Ask the court office about any final steps. Store the file, including the notice, statement, remittances, and proof of delivery.

If you receive another notice for the same debtor, repeat the process. Do not assume the first notice covers the new one. Review the new notice, file a new statement, and set up remittances if required.

If you need to amend the form later, use the same file number. Label the document as an updated statement. Cite the date of your original filing. Keep both versions and your proof of delivery.

At every step, keep your process simple. Read the notice. State facts clearly. Pay as instructed. Document everything. This approach protects you and ensures compliance.

Disclaimer: This guide is provided for informational purposes only and is not intended as legal advice. You should consult a legal professional.