Request for Mortgage Funds – Confirmation of Mortgage Registration

Fill out nowJurisdiction: Country: Canada | Province or State: Ontario

What is a Request for Mortgage Funds – Confirmation of Mortgage Registration?

This form is a lawyer-prepared request to a lender to release mortgage money. It confirms that the mortgage has been registered on title. It sets out the mortgage details, the property information, and your undertakings as the lawyer. It also tells the lender how much to send, when to send it, and where to send it. Think of it as the bridge between registration and funding. You show the lender the mortgage is properly on title and ask for the funds tied to that registration.

Who typically uses this form?

In Ontario, a lawyer or law clerk in a real estate practice prepares and signs it. You would use it when you act on a purchase, refinance, switch, or private mortgage. Sometimes the lender’s own lawyer prepares a version. More commonly, the borrower’s lawyer prepares it under lender instructions.

Why would you need this form?

Lenders need clear proof that their mortgage is registered before they release funds, or a strong, enforceable undertaking if they agree to fund before registration finishes. This form gives that proof and the related details. It also gives the lender confidence on priority, insurance, taxes, identity, and title status. Without it, you often cannot get money to close.

The typical usage scenarios

On a purchase, you register the transfer and mortgage. You then send this form with the registration particulars and ask for the mortgage advance. On a refinance, you register the new mortgage, and sometimes discharge the old one, then request funds to pay out the existing lender and other liens. On a switch, you confirm registration of the new mortgage and request funds to pay off the prior lender. For private lending, you often cannot get funds until you confirm registration and priority. The form also supports staged advances, such as construction draws, where you confirm each new registration or lien status and request the next draw.

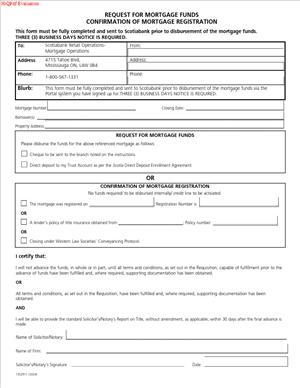

The document normally includes a confirmation of registration date and time, the instrument number, the registered amount, and the legal description. It confirms the mortgage terms match the lender instructions. It includes your undertakings to hold funds in trust and to use the money only as authorized. It often attaches your schedule of payouts and your wire instructions. It may also confirm title insurance, tax status, insurance binder, and spousal or guarantor documentation. In short, it ties together the key risk items so the lender can safely fund.

When Would You Use a Request for Mortgage Funds – Confirmation of Mortgage Registration?

You use this form any time a lender requires proof of registration or a binding undertaking before releasing mortgage money. The most common events are the day of closing on a purchase or the day you complete a refinance. In a purchase, you finalize the transfer, then register the mortgage. Once registered, you complete this form and confirm instrument details and priority. You send it to the lender with your funds direction so the lender can wire the money into your trust account. That lets you pay the seller and close.

In a refinance, timing can be tight. You may need to secure registration of the new mortgage early in the day. Once you have the instrument number, you send this form to request the funds. You include payout statements for the existing mortgage and any secured debts. The lender relies on your undertakings to apply funds first to those payouts. You then receive the wire and complete the discharges and reporting.

Some lenders allow funding on undertakings before registration confirmation. In those cases, you still complete this form, but you confirm that you will register without delay and provide registration particulars immediately after. You also undertake to return funds if you cannot perfect the mortgage with the intended priority. This is common when registration must occur late in the day, and you cannot wait for a wire after cut-off times. The lender relies on the form and your undertakings to authorize release earlier in the day.

In private lending, many lenders require strict proof. You usually complete registration first. You then send this form, along with insurance and title coverage confirmation, to trigger funding. If the lender is cautious about priority, you also provide a same-day title sub-search result and a statement that there are no new encumbrances.

Commercial deals and construction draws also use this form. For commercial properties, you may need to confirm specific covenants, assignment of rents, and environmental or zoning confirmations. For construction draws, you confirm that registration remains in force, that lien searches are clear or managed, and that required holdbacks are in place. Each draw is then requested with a new form or an update that confirms current title status.

The typical user is you, the Ontario lawyer responsible for closing. A law clerk may prepare the form, but you sign it and give the undertakings. Mortgage brokers and agents do not complete this form. The lender relies on a lawyer’s signature and trust account details. That focus reflects the risk attached to releasing large amounts of money based on registration and title priority.

Legal Characteristics of the Request for Mortgage Funds – Confirmation of Mortgage Registration

This document is not a statute-based government form. It is a legal request and a set of undertakings from you to the lender. It is binding because the lender advances funds relying on your statements and promises. Your signature creates professional and contractual obligations. If you misstate facts or breach an undertaking, you and your firm face liability. The lender can rely on the form as part of the closing record.

Enforceability comes from three parts. First, your undertakings are clear and specific. You promise to hold funds in trust, use them only for the stated purpose, and protect the lender’s priority. Second, you confirm facts that are verifiable. You provide the registration instrument number, registration time, and legal description. You attach or refer to evidence like insurance confirmation and payout statements. Third, the mortgage registration itself is public and authoritative. The lender’s charge appears on title in the stated amount and rank. Your form links the lender’s advance to that registered interest.

The form also addresses risk areas that matter for enforceability. You confirm you will pay out prior mortgages and liens from the funds. You confirm you have taken reasonable steps to verify identity. You confirm you will obtain and deliver title insurance naming the lender. You confirm property taxes are current, or you hold back enough to pay them. You confirm you will correct any registration error at your cost. These promises secure the lender’s position if issues arise after funding.

You should also consider conflicts and representation. If you act for the borrower and the lender, follow all lender instructions and obtain any required consents. If you act only for the lender, make sure the borrower has separate counsel or has waived independent advice if permitted. The form should match your actual role. Do not certify facts you cannot verify.

Privacy and trust accounting matter too. Only include the personal information necessary to identify the parties and property. Send the form over secure channels. Confirm the lender’s wiring details and authorized contacts. Hold mortgage funds in your trust account and disburse only as you disclosed. Keep records of all disbursements and confirmations.

Finally, recognize timing risks. Registration and funding often occur on the same day. You may rely on title insurance for “gap” coverage if the registration queue delays completion. If you do, say so in the form and confirm that coverage is in place. Clear, accurate statements protect both your client and your firm.

How to Fill Out a Request for Mortgage Funds – Confirmation of Mortgage Registration

Follow these steps. Keep your answers precise and consistent with the lender’s instructions.

1) Gather lender instructions and your file details

- Obtain the lender’s written instructions and conditions. Note the required documents, insurance, and any holdbacks.

- Confirm the mortgage amount, rate, term, amortization, payment frequency, and whether it is a standard or collateral charge.

- Confirm if the lender requires registration confirmation before funding, or will fund on undertakings.

- Collect borrower identification, property tax information, insurance binder, payout statements, and title insurance details.

- Have your trust account wire details ready.

2) Complete the file header and contact details

- Insert your firm name, file number, and your direct contact information.

- Insert the lender’s name, mortgage reference number, and the lender contact who will authorize funding.

- Add the requested funding date and the deadline for same-day wires if applicable.

3) Identify the parties

- List all borrowers as they appear on title. Use full legal names. Include spousal status if required by the lender.

- If there is a guarantor, list full legal name and confirm that the guarantor has signed the guarantee and any independent advice certificate.

- If a corporation is the borrower, include the legal name, incorporation jurisdiction, and signing officer details. Confirm authority to grant a charge over real property.

4) Describe the property

- Provide the municipal address and unit information if a condo or multi-unit property.

- Provide the legal description as it appears on the parcel register or deed. Keep it exact.

- Include the property identifier number, if available.

- State whether the property is freehold, condominium, or leasehold. If leasehold, confirm the lease permits a mortgage.

5) Confirm registration particulars

- State the type of instrument registered (for example, a Charge/Mortgage of Land).

- Provide the instrument number, registration date, and registration time.

- Confirm the registered mortgage amount matches the lender’s commitment.

- Confirm the chargee name matches the lender’s legal name in the instrument.

- State the intended priority (for example, first ranking). If not first, identify permitted encumbrances.

- Confirm registration of any required ancillary instruments (for example, transfer, assignment of rents, or postponements). Provide their instrument numbers if applicable.

6) Set out mortgage terms and standard charge terms

- Confirm the interest rate type (fixed or variable) and the current rate, if applicable.

- Confirm the term length, amortization period, and payment frequency.

- Identify any standard charge terms number and confirm it matches the lender’s requirements.

- Note any special covenants or schedules that were registered with the mortgage.

7) Title and priority confirmations

- State that you conducted a title search to the required date.

- Confirm there are no encumbrances ahead of the lender’s mortgage, other than those the lender has approved.

- If there are prior mortgages or liens being paid out, list each with the payout amount and creditor name.

- Confirm you will register any necessary discharges or obtain postponements.

- Confirm that title insurance is in place for the lender, effective on registration, including coverage for registration gap and priority.

8) Tax, insurance, and occupancy details

- Confirm the current status of property taxes. If there are arrears, state the holdback or the payment you will make from funds.

- Confirm you have an insurance binder with adequate coverage. Identify the lender as first loss payee under the standard mortgage clause. Confirm the policy is effective on closing.

- State the intended use or occupancy (owner-occupied, rental, or commercial). If required by the lender, confirm compliance with use restrictions.

9) Identity verification and signing confirmations

- Confirm you verified the identity of each signing party under acceptable standards.

- Confirm all mortgage documents were properly signed, witnessed, and, if needed, commissioned.

- If spousal consent or separation agreements were required, confirm completion and inclusion in your file.

- If a guarantor is involved, confirm that the guarantor received and signed required documents. Include any independent legal advice confirmations if required.

10) Disbursements and payouts schedule

- Set out a clear schedule of funds. Include:

- Total mortgage advance requested (gross).

- Less lender fees, if deducted by the lender.

- Less your legal fees and disbursements, if the lender allows you to deduct from the advance.

- Payouts to existing mortgages or secured creditors with exact amounts and account numbers if required.

- Payments for property taxes, utilities, or condo arrears if applicable.

- Title insurance premium and registration fees.

- Net funds to seller’s lawyer (in a purchase) or net balance to borrower (in a refinance), if permitted.

- Make sure the math ties to the statement of adjustments or refinance ledger.

11) Funding instructions

- Provide your trust account name exactly as registered.

- Provide the financial institution, transit, and account number, or a void cheque image if allowed.

- Provide wire instructions, including reference details so you can trace the incoming funds.

- State the requested funding date and any time constraints for same-day closing.

- Confirm that you will hold funds in trust and disburse only in accordance with lender instructions and the schedule you provided.

12) Undertakings and confirmations

- Undertake to:

- Use funds only for the stated purposes and in the order set out in the payouts schedule.

- Secure and maintain first priority (or stated priority) for the mortgage.

- Pay out and obtain discharges for any prior mortgages or liens listed.

- Deliver proof of payouts and registered discharges when available.

- Deliver the final title insurance policy and your final report within the timeline required by the lender.

- Rectify any registration errors at your cost.

- Return funds immediately if conditions for funding are not met.

- If the lender funds before registration confirmation, add a specific undertaking to register the mortgage without delay and to provide the instrument number and time immediately after. State that you will not release funds to any party until you complete registration and confirm priority, unless the lender has expressly permitted an exception.

13) Attachments and enclosures

- Attach a copy of the registration confirmation page or instrument details for the mortgage.

- Attach a copy of the insurance binder or certificate showing the lender as loss payee.

- Attach payout statements that support the disbursement amounts.

- Attach your draft statement of adjustments (purchase) or refinance ledger (refinance).

- Attach any required affidavits, spousal consents, corporate resolutions, or guarantees.

- If title insurance is used, attach the binder or coverage confirmation naming the lender.

14) Review for consistency and compliance

- Cross-check every figure against the lender’s commitment and your ledger.

- Confirm names match across all documents. Check spelling and capacity for corporations.

- Confirm the legal description and instrument number exactly match the registry.

- Ensure your undertakings match the lender’s funding conditions. Do not promise what you cannot perform on closing day.

- Verify your trust account details and wire instructions are current and accurate.

15) Signatures and authorization

- Insert the place and date of signing.

- Sign the form as the lawyer responsible for the file. Print your name beneath the signature.

- Include your lawyer licence number and firm address and contact details.

- If the lender requires a countersignature or authorization code, obtain it and record the name of the lender representative who approves release.

16) Submission and follow-up

- Send the form and attachments to the lender’s funding department or designated contact using the secure method they require.

- Call or message to confirm receipt and readiness to fund. Note the expected wire time.

- Monitor your trust account for the incoming wire. Confirm the reference matches.

- Once funds arrive, disburse in the order you disclosed. Keep receipts and confirmations.

- After closing, send your final report and any outstanding registration or insurance documents by the deadline.

Practical example: purchase with same-day funding. You register the transfer and mortgage at 10:30 a.m. You complete this form, insert the instrument number, and confirm first priority. You attach the insurance binder and adjustments. You request funds for 1:00 p.m. You receive the wire at 12:45 p.m., then send the closing funds to the seller’s lawyer. You deliver the final report and policy within the lender’s timeline.

Practical example: refinance with payout and tax arrears. You register the new first mortgage at 9:15 a.m. You prepare this form showing two payouts: the prior lender and condo arrears. You hold back an amount to clear property tax arrears. You receive the wire and immediately pay the prior lender and condo corporation. You order the discharge of the old mortgage and send proof to the new lender with your final report.

A few closing tips. Use clear numbers and avoid ranges. If a payout statement has a per diem, include the per diem and the date through which you calculated. If you rely on title insurance for gap coverage, say so. If you need a specific holdback, explain the reason and the release conditions. And always match the lender’s instructions word for word on conditions and naming. That detail speeds funding and prevents last-minute delays.

Legal Terms You Might Encounter

Mortgagor (Borrower): This is your client granting the mortgage. On the form, you confirm their legal name matches the registered charge and the identification you verified.

Mortgagee (Lender): This is the funder receiving your request. On the form, you identify the lender exactly as shown in the registered mortgage to avoid funding delays.

Charge/Mortgage of Land: This is the registered instrument that secures the loan. Your confirmation states that the charge is registered for the correct amount and terms.

Registration and Instrument Number: Registration means the charge is filed on title. The instrument number is the unique identifier. You include this number on the form so the lender can verify the registration.

Legal Description and Property Identifier (PIN): The legal description and PIN identify the parcel charged. You confirm these details match the mortgage instructions and the registered charge.

Priority and Postponement: Priority determines who gets paid first on enforcement. If another encumbrance sits ahead, a postponement or discharge is needed. On the form, you confirm that the lender has the required priority.

Interest Adjustment Date (IAD): This is when regular interest calculations start. It often follows funding. You note the IAD on the form so the lender can set up interest and payments.

Holdback: A holdback is money you retain for specific reasons, such as taxes, repairs, or undertakings. You show the holdback amount and purpose in your disbursement details.

Solicitor’s Undertaking: This is your professional promise to complete post-closing steps. You may request funds on your undertaking to register, obtain discharges, or deliver documents. The form records any undertakings tied to funding.

Direction re Funds and Disbursements: This sets out who gets paid and how. You itemize payouts, fees, and net proceeds. The form confirms your trust account details and the exact amounts you will disburse on closing.

Payout Statement and Discharge: A payout statement shows the amount to retire an existing mortgage or lien. You confirm you will pay and obtain any required discharge. The form reflects these amounts in your disbursement plan.

Title Insurance: Title insurance protects against certain title risks. Many funders require it. You confirm issuance and policy details on the form, so the lender’s risk conditions are satisfied.

FAQs

Do you need to register the mortgage before sending the request for funds?

You should follow the lender’s instructions. Many lenders require the instrument number and priority confirmed before releasing funds. Some allow funding on your undertaking to register immediately and deliver proof after. If funding on undertaking, state your undertaking clearly on the form.

Do you need the instrument number to complete this form?

In most cases, yes. The instrument number lets the lender confirm the charge on title. If you are requesting funds before registration, explain why and provide your undertaking. Update the lender with the instrument number as soon as it is available.

Do you need original ink signatures, or are e-signatures acceptable?

It depends on the lender and the document. Many lenders accept e-signatures for certain documents. Some still require wet signatures for key mortgage forms. Check the lender’s instructions and flag any e-signature use in your cover note.

Do you have to provide proof of insurance with this request?

Yes, usually. Lenders often require evidence of property insurance with their loss payable wording. Attach the binder or proof. Note the insurer, coverage, and policy term on the form or in your cover note.

Do you need to include title insurance details?

Often, yes. Many lenders require title insurance for both lender and borrower coverage. Confirm policy details and premium on closing. If the policy will issue post-closing, provide your undertaking and expected delivery date.

Do you need to confirm property taxes are up to date?

Lenders typically require tax status. If taxes are unpaid, you may need a holdback or payment on closing. Reflect any holdback or payment in your disbursement summary and note the plan in your cover letter.

Do you need to update the form if the funding date or amounts change?

Yes. Send a revised request if the closing date, IAD, disbursements, or holdbacks change. Confirm any revised totals and explain the reason for the change. Ask the lender to reconfirm release timing.

Checklist: Before, During, and After the Request for Mortgage Funds – Confirmation of Mortgage Registration

Before you sign or submit

- Confirm client names match identification and the registered charge.

- Verify the legal description and PIN match the property being mortgaged.

- Ensure the charge amount, interest rate, term, and IAD match instructions.

- Obtain the instrument number or prepare a clear undertaking if pre-registration funding is needed.

- Secure title insurance arrangements and note policy details or undertakings.

- Review property tax status; set any required holdback or payment.

- Gather insurance proof with lender loss payable wording.

- Obtain payout statements for existing mortgages or liens with valid per diem.

- Confirm any required postponements, discharges, or consents are ready.

- Prepare the statement of adjustments and the direction re funds.

- Confirm trust account details for receiving and disbursing funds.

- Review lender conditions and outstanding requirements one by one.

- Verify wiring instructions and any security controls with the lender.

- Confirm signing logistics and borrower availability for closing.

- Prepare your undertakings and a delivery plan for post-closing items.

During review and signing

- Check the lender and borrower names exactly as registered.

- Confirm the instrument number, registration date, and land registry references.

- Verify the property address, legal description, and PIN on all pages.

- Confirm the mortgage amount, interest rate, term, and IAD.

- Review any special conditions or covenants noted on the charge.

- Verify payouts, per diems, and total disbursements match the direction re funds.

- Confirm holdback reasons, amounts, and expected release conditions.

- Ensure title insurance details are correct or undertakings are recorded.

- Confirm insurance binder details and coverage start date.

- Review your undertakings stated in the form for accuracy and scope.

- Recalculate totals to ensure the math balances to the requested funds.

- Confirm signing dates align with the planned funding date.

After submission and funding

- Send the executed form and required attachments to the lender.

- If funded on undertaking, complete registration and deliver proof promptly.

- Pay out existing mortgages and liens from trust and secure discharges.

- Satisfy any conditions tied to holdbacks and track release dates.

- Deliver final, signed copies of the charge and supporting documents.

- Provide title insurance policy documents to the lender and client.

- Remit property taxes or set up a tax account per lender requirements.

- Confirm receipt of funds and reconcile the trust ledger the same day.

- Send the lender a concise post-closing report and disbursement summary.

- Store registration receipts, payout proofs, and wire confirmations.

- Diarize renewal, IAD, and any post-closing delivery deadlines.

- Update your client with a closing memo and copies for their records.

Common Mistakes to Avoid

Wrong instrument number or property identifier. A single digit error can stall funding. Don’t forget to copy the instrument number directly from the registry receipt and verify the PIN.

Mismatch between lender instructions and the registered terms. Funding can be refused. Don’t forget to cross-check the charge amount, rate, term, and IAD before you submit.

Missing priority arrangements. The lender may lack first security. Don’t forget to obtain and record postponements or discharges when another encumbrance sits ahead.

Incomplete insurance or title insurance proof. Funds can be held back. Don’t forget to attach the insurance binder and confirm title insurance issuance or undertakings.

Inaccurate disbursement totals. Trust shortages create risk and delays. Don’t forget to reconcile payouts, fees, and holdbacks, and ensure the math balances to the request.

What to Do After Filling Out the Form

Confirm delivery and receipt. Send the signed form with all attachments. Ask the lender to confirm receipt and release timing. If a portal is used, upload and verify status.

Complete registration or post-closing undertakings. If you funded on undertaking, register the charge immediately and send the instrument number and receipt. Deliver any outstanding items, such as policies, confirmations, or final executed documents.

Disburse funds from trust as approved. Follow the direction re funds exactly. Pay out existing mortgages and liens using current payout statements. Pay property taxes or set a holdback if required. Document every transfer and supplier payment.

Secure priority and discharges. Obtain and register any required postponements or discharges. Send proof to the lender. Update your file index with instrument numbers and dates.

Finalize insurance and title insurance. Deliver the insurance binder or certificate with the lender’s loss payable wording. Provide the title insurance policy documents as soon as they issue. Note any endorsements and effective dates.

Report to the lender. Prepare a concise post-closing report. Include the registration details, proof of payouts, evidence of priority, and copies of key documents. Restate any open undertakings with target delivery dates.

Update the client. Send a closing memo with a simple summary. Include the registered charge, payments made, net funds, and next steps. Provide copies of signed documents for their records.

Handle amendments or corrections. If you discover an error in names, amounts, or dates, notify the lender at once. Issue a corrected form or a written addendum. If needed, prepare and register a corrective instrument. Keep a clear audit trail of changes and confirmations.

Store and diarize. Save registration receipts, payout proofs, confirmations, and correspondence. Diarize the IAD, renewal date, and any undertakings. Keep trust records complete and reconciled.

Close the loop on holdbacks. Track release conditions. Collect required receipts or clearances. Seek lender approval before releasing funds. Record the release in the trust ledger and your closing report.

Maintain compliance hygiene. Confirm identity records, conflict checks, and file notes are complete. Ensure that all lender instructions are marked as satisfied. Archive securely according to your retention policy.

Disclaimer: This guide is provided for informational purposes only and is not intended as legal advice. You should consult a legal professional.