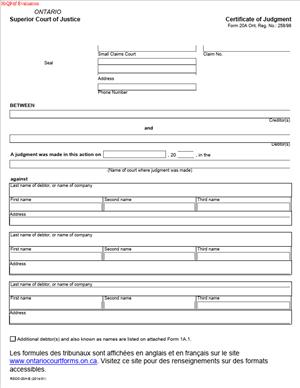

Form 20A – Certificate of Judgment

Fill out nowJurisdiction: Canada | Ontario

What is a Form 20A – Certificate of Judgment?

Form 20A is the Small Claims Court Certificate of Judgment used in Ontario. It is an official certificate prepared and issued by the Small Claims Court clerk after a judgment or order for money. The certificate confirms the key terms of your judgment, including who owes what, interest, and the court file details. You use it to take enforcement steps outside the Small Claims Court office, especially with the sheriff’s enforcement system.

Think of it as the court’s stamped summary of your win. The judgment itself grants your rights. The certificate makes those rights portable, so you can register and enforce the debt in places that need a certified record.

Who typically uses this form?

Judgment creditors do. That includes individuals, landlords, tenants, tradespeople, contractors, professionals, insurers, and businesses of all sizes. Lawyers and licensed paralegals use it often. Self-represented litigants use it too. The debtor does not complete this form.

Why would you need it?

Some enforcement tools sit outside the Small Claims Court office. For example, if you want to register a writ against the debtor’s land, you work through the sheriff’s enforcement office tied to the Superior Court of Justice. That office will expect a certified record of your Small Claims judgment. Form 20A is that record. The same applies if you plan to enforce in another region or need a sealed court certification to support searches or collections steps.

Typical usage scenarios

- You won a judgment for unpaid rent. The debtor will not pay. You want to register a writ against any land the debtor owns. You obtain Form 20A, then take it to the sheriff’s enforcement office to issue and file your writ.

- You won a judgment against a contractor who owns a home in another region. You need a certified record to register a writ in that region. You get Form 20A, then file the writ where the home is located.

- Your business won a default judgment. The debtor has assets outside your local court’s territorial division. You need Form 20A to bring the judgment into the sheriff’s system and search for assets.

- You want to record the debt in a way that shows up on land title searches. You use Form 20A to issue and file a writ. The writ can then be indexed against the debtor’s name.

In short, Form 20A puts your Small Claims Court judgment into the broader enforcement stream. It converts your win into an enforceable tool with the sheriff.

When Would You Use a Form 20A – Certificate of Judgment?

You use Form 20A after you have a final money judgment or order in Small Claims Court. You do not use it before judgment. It follows a default judgment, a judgment after a hearing, or a consent judgment. It can also follow an order that sets the amount payable, even if the case settled.

Use it when you want to enforce beyond basic in-office tools. For example, if you plan to register a writ of seizure and sale of land, the sheriff will expect a certified judgment. The sheriff’s office is part of the Superior Court enforcement system, not the Small Claims office. The certificate bridges that gap.

If your enforcement stays within Small Claims Court processes only, you may not need the certificate. For example, if you plan to start garnishment through the Small Claims Court clerk, that process occurs within that office. But many creditors want to pressure payment by registering a writ against land. That step needs the certificate.

You also use the certificate when the debtor’s assets, business, or land are in another county or region. You can obtain one certificate and use it to issue writs in multiple enforcement offices. You might also need a current certificate if time has passed and interest has grown. The certificate ensures any enforcement office sees an accurate, certified balance.

Typical users include small landlords seeking rent arrears, residential tenants seeking return of deposits, contractors unpaid for work, retailers owed for goods, professionals with unpaid invoices, and consumers with judgments against businesses. It is also used by collection agencies and assignees of judgment debts. If you are trying to locate or seize assets through the sheriff’s system, you will almost always need Form 20A first.

You would not use it to appeal, set aside, or change a judgment. It is not a motion form. You also avoid using it if the judgment is stayed, suspended, or paid in full. If the court granted a time-to-pay schedule, follow that order first. Once the debtor defaults and the order allows enforcement, you can proceed with the certificate.

Legal Characteristics of the Form 20A – Certificate of Judgment

Form 20A is an official certificate issued by the Small Claims Court. It is not the judgment itself. It is the court’s certified statement of that judgment. Its legal strength comes from the court’s seal, the clerk’s signature, and the match between the certificate and the court’s record. Enforcement offices rely on it because it is an authoritative court record.

It is legally effective because court rules allow enforcement of Small Claims judgments through the sheriff’s system when properly certified. The certificate confirms the key details: parties, file number, date of judgment, amounts, interest, and the current balance. It also confirms that the judgment stands and has not been vacated on the face of the court record. That allows you to issue writs in the enforcement office.

Enforceability depends on accuracy and status. The amounts in the certificate must track the actual judgment and any later orders that changed it. If the debtor has made partial payments, the certificate must reflect the credits and the correct balance. Interest must be calculated under the rate in the judgment or under the default rules that apply. If the judgment is stayed by an appeal or order, you cannot enforce. If a stay exists, you should not obtain or use the certificate to start enforcement.

The certificate does not expire on a set date, but the writs you issue from it do. Writs carry a lifespan and renewal rules. If significant time passes, you may need a new certificate to show the updated balance and interest. Many creditors do that to keep records clean and avoid confusion across offices.

The names in the certificate matter. The writ will index against the debtor’s name. If the judgment debtor uses multiple names, include them as set out in the case. If the debtor is a corporation, match the exact corporate name. If an individual uses a business name, ensure the style of cause shows both. Precise names improve the writ’s effect on land searches and asset matching.

If the judgment is joint and several, the certificate will show the total amount owing. You can enforce against any debtor, subject to exemptions and priority rules. If the court allocated liability between defendants, reflect that detail. The enforcement office will rely on the certificate to know who owes which share.

Finally, the certificate supports credibility for searches. Title offices and judgment searches will accept a writ issued from a certified judgment as notice of debt. That is why the court seal and signature are essential. They validate the judgment for third parties who were not in your case.

How to Fill Out a Form 20A – Certificate of Judgment

Follow these steps. Take your time. Accuracy matters. Keep copies of everything you file.

1) Confirm you have a final, enforceable judgment

- Read the judgment or order. Confirm it awards money.

- Ensure there is no stay of enforcement.

- Note the date of judgment and the judge or deputy judge.

- Note any later order that changed the amount, rate, or terms.

2) Gather the information you need

- Court file number and the Small Claims Court location.

- Names of all judgment creditors and debtors, exactly as on the case.

- Full mailing addresses for the parties.

- The principal amount awarded, costs awarded, and any pre-judgment interest.

- The post-judgment interest rate, if stated, or the default rate that applies.

- Any payments received since judgment and the dates.

- Your current balance and a per diem interest amount.

3) Start the form with court and party details

- Enter the court file number exactly as it appears in your case.

- Enter the Small Claims Court address and location name.

- List the creditor(s) and debtor(s) as shown on the judgment.

- Include all known aliases or business styles that appear in the case.

- Use legal names. Avoid nicknames. Match capitalization and punctuation.

4) Insert the judgment details

- Enter the date of judgment and the name of the judge or deputy judge.

- State the original amounts: damages or debt, costs, and pre-judgment interest.

- Identify any later order that changed the amounts. If so, note the date and effect.

- If your judgment includes a schedule or terms, reference them as needed.

5) Calculate and state the current balance

- Start with the principal and costs from the judgment.

- Add any pre-judgment interest awarded up to the judgment date.

- Add post-judgment interest from the judgment date to today, at the correct rate.

- Subtract any payments received after judgment. List payment dates and amounts.

- State the current total owing as of today’s date.

- Provide a per diem interest amount. Calculate as: current principal subject to interest × rate ÷ 365. If the judgment sets a different method, follow that.

Practical tip: Be precise about what portion bears interest. Sometimes costs bear interest. Sometimes they do not. Follow the wording of your judgment.

6) Identify the interest rate and basis

- If the judgment sets a specific post-judgment rate, enter that rate.

- If not, use the default post-judgment rate that applies.

- If the rate changed due to an order, note the change and effective date.

- If pre-judgment interest was awarded at a specific rate, show it as well.

7) Note any credits, set-offs, or adjustments

- If the debtor paid part of the judgment, itemize each payment.

- If there were returned payments or chargebacks, explain briefly.

- If the court allowed a set-off or variation, reflect it and cite the order date.

8) Add debtor identification detail, if space allows

- Include middle names or initials that appear on the court record.

- Include known addresses to help differentiate between similar names.

- If the debtor is a corporation, confirm the exact corporate name.

While Form 20A focuses on certified judgment details, clear names improve enforcement later. If the form has limited space, use the exact style of cause and consider an attached schedule for clarity.

9) Attach schedules if needed

- Use a Schedule A for party names if there are many debtors or creditors.

- Use a Schedule B for a detailed interest and payment calculation.

- Label each schedule with the court file number and case name.

- Keep the schedules clean and easy to follow. Avoid complex formulas.

10) Review for accuracy and consistency

- Cross-check amounts against the judgment and any later orders.

- Verify spelling of names and addresses.

- Confirm that interest calculations are correct to the date on the form.

- Ensure totals add up. Small math errors trigger delays.

11) File the form with the Small Claims Court for certification

- Bring the completed form to the Small Claims Court office where the judgment was made.

- Ask the clerk to issue and sign the certificate. A fee applies.

- The clerk will compare your entries with the court record.

- Be prepared to show the judgment and any later orders.

- If your math is unclear, the clerk may ask for a breakdown or revisions.

12) Obtain the signed and sealed certificate

- The clerk will sign and affix the court seal.

- Ask for several certified copies. You will need them for enforcement offices.

- Keep a digital scan for your records.

13) Use the certificate to enforce

- Take the certificate to the sheriff’s enforcement office to issue your writ.

- File in every region where the debtor may own land or assets.

- Follow the enforcement office’s filing process and pay required fees.

- Keep your certificate copies safe. You may need to issue additional writs later.

14) Keep your balance current

- Track payments received after certification.

- If the debtor pays part of the balance, update your records immediately.

- Before issuing a new writ, consider obtaining a fresh certificate that shows the current balance and interest.

15) Consider practical naming and search issues

- For individuals, exact names and dates of birth reduce mis-hits, though dates of birth are usually not on Form 20A. The writ process may collect them.

- For corporations, confirm the legal name and any numbered company suffix.

- If the debtor used a business name, make sure your style of cause shows both the individual and the business name as applicable.

16) Watch for stays or changes

- If the debtor files a motion to set aside or appeals with a stay, pause enforcement.

- If the court varies the judgment, obtain an updated Form 20A.

- If the judgment is satisfied, do not enforce further. You may have a duty to withdraw or note satisfaction on writs.

Common pitfalls to avoid:

- Entering the wrong interest rate. Always check the judgment first.

- Forgetting to subtract payments. Keep a ledger.

- Using a nickname or short form for the debtor’s name.

- Mixing pre-judgment and post-judgment interest periods.

- Certifying too early if the order provides time-to-pay and no default yet.

Real-world example:

You won $12,500 plus $500 costs on March 1. The judgment sets post-judgment interest at the default rate. The debtor paid $2,000 on April 15. Today is September 1. You prepare Form 20A. You list the principal and costs, show the one payment, and calculate post-judgment interest from March 1 to September 1 on the unpaid principal (plus interest on costs, if allowed by your order). You present the form to the clerk, who certifies it. You make three certified copies. You then issue writs in two regions where the debtor might own land. You keep one certificate in your file.

Another example:

You have a consent judgment that includes a payment schedule. The debtor misses two payments and the consent terms allow immediate enforcement on default. You calculate the balance, update interest to today, and obtain Form 20A. You file it with the sheriff to register a writ, which places pressure on the debtor to pay or refinance.

Final tips:

- Keep sentences short and calculations transparent. Enforcement offices appreciate clarity.

- Do not guess interest rates. Confirm them.

- If the debtor’s name changed, ensure the style of cause matches the judgment. Later enforcement can add name variants when permitted.

If you follow these steps, your Form 20A will be accurate, certified, and ready to support enforcement. That saves time, reduces return trips to the counter, and moves your file toward collection.

Legal Terms You Might Encounter

A judgment is the final decision that states who owes what. Your certificate confirms that decision in a standard format. It shows the amount and the date so enforcement offices can act.

The judgment creditor is the person or business who won. You are the creditor if the court ordered payment to you. The certificate identifies you as creditor so writs and searches point to you.

The judgment debtor is the person or business who owes money. The form lists each debtor by full legal name. Exact names matter for enforcement and asset searches.

Post‑judgment interest is the interest that accrues after the judgment date. The certificate shows the rate and calculation date. This lets enforcement offices accept your total.

Pre‑judgment interest may be part of your judgment. If the court awarded it, the certificate reflects that amount. You cannot add pre‑judgment interest that was not awarded.

Costs and disbursements are court‑ordered amounts for your fees and expenses. The certificate includes them only if the court awarded them. Do not add costs that are not in the judgment.

Enforcement is the legal process to collect. The certificate is your bridge to enforcement offices. It proves the judgment so you can request writs or other measures.

A writ is a command to an enforcement office to act. With a certificate, you can file for a writ against land or personal property. The writ uses the certificate as the source record.

Garnishment is a way to collect from wages or bank accounts. A certificate is often not required for a garnishment started in Small Claims Court. It is useful when you register the judgment elsewhere.

A stay is a court order that pauses enforcement. If a stay exists, the certificate should not be used to enforce. You must wait until the stay is lifted or expires.

Satisfaction of judgment means the debt is paid. When paid, you should update the court record. You should also stop enforcement and, when needed, release writs or garnishments.

An amendment is a correction or update to a court document. If the certificate has an error, ask the clerk for an amended version. Use the amended certificate for future filings.

FAQs

Do you need a Certificate of Judgment to issue a writ?

Yes. If you plan to file a writ with an enforcement office, you need the certificate. It confirms the judgment details and amounts so the writ can be registered and enforced.

Do you include post‑judgment interest on the certificate?

Yes. The certificate shows the interest rate and the date through which interest is calculated. Update the interest amount to the date you request enforcement. Keep your math clear and traceable.

Do you need a separate certificate for each debtor?

You typically use one certificate for the case that lists all debtors. Make sure each debtor’s full legal name appears exactly as on the judgment. If names differ, discuss an amendment with the clerk.

Do you have to serve the debtor with the certificate?

Usually, no. The certificate is used to register and enforce the judgment. Service rules apply to the enforcement steps you take, not to the certificate itself. Follow the service rules for each enforcement method.

Do certificates expire?

The certificate is proof of a valid judgment. Enforcement tools have timelines and renewals. Writs and garnishments have their own expiry rules. Track those dates and renew as required.

Do you need multiple originals?

It is wise to obtain more than one sealed original. You may need to file in different enforcement offices. Ask the clerk for extra sealed copies when you request issuance.

Can you correct an error after the certificate is issued?

Yes. If you spot a clerical error, request an amended certificate from the clerk. Use the corrected version for any new filings. If you already filed a writ, ask the enforcement office how to update the record.

Can you use the certificate outside your court’s area?

Yes. The certificate helps you register the judgment where the debtor has assets. File in any enforcement office where you need to act. You may need extra copies for each location.

Do partial payments affect the certificate?

Yes. The certificate states the judgment amount and payments to date. Update payments and interest when you request enforcement. Do not enforce for amounts already paid.

Do you need the debtor’s birth date or identifiers?

They help enforcement offices match the debtor to assets. If you have them, include them where the form allows. If not, provide any identifying details you can confirm.

Checklist: Before, During, and After

Before signing

- Judgment or order details: date, amounts, and any costs.

- Parties’ exact legal names, including spelling and punctuation.

- Addresses for each debtor and creditor.

- Any known aliases or operating names for the debtor.

- Interest information: rate, start date, and calculation method.

- Record of payments made after judgment.

- Your file number and the court file number.

- Proof of authority if you sign for a company or as agent.

- Extra copies request, if you plan to file in multiple places.

- Payment method for court fees, if applicable.

During signing

- Confirm the court location and correct file number.

- Verify the judgment date and type match the court record.

- Check each party’s full legal name against the judgment.

- Enter the principal, costs, and pre‑judgment interest as awarded.

- Calculate post‑judgment interest to a specific date.

- Deduct any payments already received from the total.

- Ensure the totals add up and are easy to follow.

- Confirm any identifying details for the debtor are correct.

- Review for typos and missing fields.

- Sign in the right spot and date the form.

After signing

- File the form with the Small Claims Court clerk to be sealed.

- Request extra sealed originals for multiple filings.

- Review the sealed certificate for stamp, seal, and accuracy.

- Choose your enforcement path based on known assets.

- File the sealed certificate with the enforcement office if needed.

- Keep a copy of everything you file and receive.

- Record dates, fees, and interest calculations in your file.

- Notify the debtor as required for your chosen enforcement step.

- Update your ledger with any new payments received.

- Store documents securely for quick access and audits.

Common Mistakes to Avoid

Using the wrong debtor name. If the name does not match the judgment, enforcement can fail. Don’t forget to use the exact legal name and any known aliases from the record.

Adding amounts not awarded. If you include fees or costs the court did not award, you risk rejection or challenges. Don’t include extras unless they appear in the judgment.

Interest miscalculations. Wrong rates or dates can block enforcement or reduce recovery. Don’t forget to show your interest period and rate, and check the math.

Out‑of‑date payment totals. Enforcing for money already paid can lead to disputes and set‑offs. Don’t forget to subtract all payments received, with dates.

Submitting an unsigned or unsealed certificate. Enforcement offices need a signed and sealed certificate. Don’t forget to confirm the clerk’s seal and signature are present before you file.

Proceeding despite a stay or appeal. Enforcement during a stay can be set aside and may cost you. Don’t forget to confirm the judgment is enforceable on the filing date.

What to Do After Filling Out the Form

- File the certificate for sealing. Take your completed form to the Small Claims Court clerk. Ask for the certificate to be issued and sealed. Request extra sealed copies if you plan to file in more than one place.

- Confirm accuracy after issuance. Check the court seal, signature, names, dates, amounts, and interest. Make sure the sealed certificate matches your calculations and the judgment.

- Decide your enforcement route. Choose methods that fit the debtor’s assets. Consider a writ against land or personal property. Consider garnishment if you know an employer or bank. You can pursue more than one method.

- File at the right enforcement office. Use an enforcement office where the debtor has assets or lives. Provide the sealed certificate and any required forms for that office. Pay the filing fees.

- Calendar renewals and milestones. Track any expiry dates for enforcement tools. Set reminders to renew writs or continue garnishments. Note interest update dates.

- Keep the debtor’s information current. Update addresses, employers, or banking details as you learn more. Use updated information for new enforcement steps.

- Apply payments and adjust totals. Record all payments with dates. Update post‑judgment interest up to the latest payment date. Do not enforce for amounts that are no longer owing.

- Handle amendments promptly. If you discover an error in the certificate, request an amended version. Provide the amended certificate to any enforcement offices that need it.

- Coordinate filings across regions. If the debtor has assets in different areas, file sealed copies there. Keep a log of where you filed, the dates, and reference numbers.

- Close out when paid. When the judgment is satisfied, stop enforcement. Take steps to release or withdraw writs or garnishments. Update the court record to show satisfaction, if required.

Disclaimer: This guide is provided for informational purposes only and is not intended as legal advice. You should consult a legal professional.