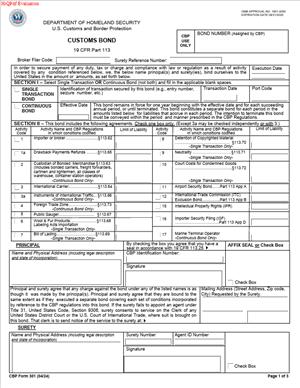

CBP Form 301 – Customs Bond

Fill out nowJurisdiction: Country: USA | Province or State: Federal

What is a CBP Form 301 – Customs Bond?

CBP Form 301 is the standard customs bond used at the federal level. It guarantees that you will follow customs laws, pay all duties, taxes, and fees, and meet all post-entry obligations tied to your imports or other customs activities. Think of it as a financial promise backed by a surety company. If you fail to comply, the government can claim against the bond to recover what’s owed.

You use this form to post either a single transaction bond for one shipment, or a continuous bond that covers your ongoing activity. The form also accommodates bonds for different customs activities beyond importing, such as operating a bonded warehouse, serving as a carrier, acting as a container station, claiming drawback, or running a foreign trade zone. The same form structure applies, with different conditions attached based on the activity you select.

Who typically uses this form? Importers of record, customs brokers acting for importers, carriers, warehouse operators, container freight station operators, foreign trade zone operators, and drawback claimants. If you import commercial goods into the United States, you will likely need this bond at some point, even for a single shipment.

You would need this form when customs requires financial coverage before it allows release of merchandise or authorizes an activity. For a standard commercial entry, customs will not release your goods until a valid bond is on file. A continuous bond also covers related obligations, such as Importer Security Filing for ocean shipments and post-entry audits or adjustments. If you operate a bonded facility, transport bonded merchandise, or seek accelerated drawback refunds, the bond is mandatory.

Typical usage scenarios include:

- You import only once or twice a year. You post a single transaction bond tied to each entry.

- You import regularly. You maintain a continuous bond so your entries, security filings, and post-entry actions stay covered without delays.

- You operate a bonded warehouse or container station. You post a custodial bond to cover your handling of bonded goods.

- You are an airline, ocean carrier, or NVOCC. You post a carrier bond to cover manifesting, arrival, and movement obligations.

- You claim drawback refunds. You post a drawback bond to secure repayment if a refund later proves improper.

- You manage a foreign trade zone. You post the relevant bond to secure zone operations and inventory controls.

At its core, CBP Form 301 is a three-party agreement. You are the principal. A surety company authorized to do business with the federal government acts as the backer. Customs is the obligee. The surety promises to pay customs up to the bond amount if you fail to meet your obligations. You then owe the surety for any amount it pays on your behalf.

When Would You Use a CBP Form 301 – Customs Bond?

You use this form when customs requires financial assurance to release cargo, allow bonded movements, or authorize a regulated activity. The most common trigger is a customs entry. If you bring goods into the U.S. for commercial use, customs needs a bond on file before it releases your shipment from its control.

If you import infrequently, a single transaction bond can be more cost-effective. It is tied to one entry, including any associated security filings for that shipment. If you import on a regular schedule, a continuous bond is practical. It eliminates the need to arrange a bond for each entry and reduces clearance delays. A continuous bond also stays in place for your post-entry obligations, such as responding to requests, paying rate advances, and handling liquidated damages claims if they arise.

You also use this form when your business handles bonded goods. For example, if you run a container freight station, you need a custodial bond to receive and hold freight under customs control. If you operate a bonded warehouse, the bond covers inventory control and withdrawals. If you move in-bond cargo from the port of arrival to another port, you or your carrier need bond coverage for that transit.

If you are a carrier, you use this form to post a carrier bond that supports your manifest, arrival, and in-bond obligations. This applies to airlines, ocean carriers, and sometimes NVOCCs, depending on your role and movements.

If you claim drawback, you use the form to post a drawback bond, especially if you want accelerated payment. The bond allows customs to pay you before it completes final verification, and it protects the government if a later review shows the claim was overstated.

If you operate a foreign trade zone, you post the applicable bond using this form. It secures your inventory control, admission, and zone procedures. The bond aligns with the activities allowed under your zone authority.

Certain special entries also rely on this form. Temporary importations under bond, or entries that require the ability to redeliver goods for inspection or marking, rely on bond coverage. If customs requires redelivery and you cannot produce the goods, the bond covers the resulting claim.

In short, if customs needs a financial guarantee to allow your activity, you will use CBP Form 301 to put that guarantee in place.

Legal Characteristics of the CBP Form 301 – Customs Bond

This bond is legally binding once customs accepts it. It is a surety bond, which means you and the surety are jointly and severally liable up to the bond amount. Customs can make a demand on the surety without first exhausting remedies against you. The surety then has recourse against you under your indemnity agreement.

Enforceability rests on several pillars. First, the form incorporates standard bond conditions for the activity you select. These conditions require you to obey customs laws, pay duties, taxes, and fees, produce documents on request, keep records, and allow inspection. They also require you to redeliver goods on demand and to comply with any special requirements tied to your activity, like inventory controls in a bonded facility. For importers, the conditions also cover marking, labeling, and other agency compliance when applicable.

Second, the bond must be issued by a surety that is authorized to write federal bonds. The surety’s attorney-in-fact must have valid power of attorney on file. Customs will not accept a bond from an unauthorized surety or an agent without proper authority.

Third, the bond must show a clear penal sum, which is the maximum liability of the surety. For continuous bonds, the penal sum is a fixed amount that remains available for all covered obligations. For single transaction bonds, the penal sum is set to cover the specific shipment’s potential liabilities. Customs can issue a claim for liquidated damages or duties, taxes, and fees up to the penal sum if you default.

The bond has staying power. Even if you cancel a continuous bond, it remains liable for entries and obligations that occurred while the bond was active. This “tail” lasts until customs closes those obligations through liquidation or final resolution. The same applies to a single transaction bond, which remains in force for the shipment it covers until all duties are final and all conditions are met.

Customs enforces the bond through formal notices. If it believes you violated a bond condition, it issues a demand for redelivery, a request for information, or a notice of liquidated damages. If you do not comply or resolve the issue, customs will issue a claim against the bond. You can respond and seek mitigation, but if the claim stands, the surety must pay up to the bond amount.

Because this is a regulated federal surety bond, the formalities matter. If any required signatures, authorities, or addenda are missing, customs can reject the bond. If the penal sum is too low for your activity, customs can demand an increase or refuse to release your goods. If your name or corporate structure changes, you must file a rider so the bond matches your legal identity. Failure to maintain accurate bond information can delay clearances and raise compliance risk.

In practice, the bond is both a clearance tool and a compliance backstop. It allows goods to move while giving customs a reliable way to recover funds and ensure adherence to the law. That is why customs takes bond sufficiency and surety authorization seriously.

How to Fill Out a CBP Form 301 – Customs Bond

Follow these steps to complete and file the bond correctly. You can do this directly with a surety or through your customs broker. Many bonds today are filed electronically, but the information you provide remains the same.

Step 1: Choose the bond structure

- Decide between a single transaction bond and a continuous bond.

- Single transaction bonds work for occasional imports or one-off activities.

- Continuous bonds fit recurring imports and ongoing activities. They cover your entries, security filings where applicable, and post-entry events during the bond’s term.

Step 2: Identify the activity and conditions you need

- Select the activity your bond must cover. Examples include importer of record, carrier, custodial operator, bonded warehouse, container station, foreign trade zone, or drawback.

- The activity drives the bond conditions that apply to you. Importer bonds emphasize payment, compliance, and redelivery. Custodial bonds emphasize custody, inventory control, and transfer rules. Carrier bonds emphasize manifesting, arrival, and in-bond movements.

- If you perform more than one activity, discuss whether to file separate bonds or add the needed conditions under one bond where permitted.

Step 3: Size the bond amount (penal sum)

- For continuous importer bonds, the penal sum is often driven by your prior year’s duties, taxes, and fees, with a regulated minimum and step-ups as exposure grows.

- For a single transaction bond, the penal sum must cover the risks tied to that shipment. Sensitive entries or entries involving special programs may require a higher amount.

- A surety or broker will help you propose a sufficient amount. Customs can ask for a higher amount if it finds the bond insufficient.

Step 4: Gather the principal’s identity and tax information

- Legal name of the principal exactly as it appears in your organizing documents.

- Type of entity (corporation, LLC, partnership, or individual).

- State or country of organization if a business entity.

- Employer Identification Number or other government-issued number used for customs identification.

- Principal address and contact details.

- If you use a trade name, include it as a DBA where allowed.

Step 5: Identify the surety and agent

- Choose a surety authorized to write federal bonds.

- You will work with an agent or broker who has a power of attorney from the surety to sign bonds.

- The bond will reference the surety’s identification code and bond number assigned by the surety.

Step 6: Complete the bond core fields

- Bond type: mark single transaction or continuous.

- Penal sum: enter the exact amount. For continuous bonds, use the fixed amount. For single transaction bonds, use the shipment-based amount.

- Effective date: for continuous bonds, select the start date. For single transaction bonds, tie the date to the entry.

- Activity and conditions: indicate the selected activity. Attach the correct condition addendum if required.

- Port or coverage: for single transaction bonds, specify the port or district associated with the entry if applicable. Continuous bonds generally show coverage for all ports.

- Entry or transaction details: for a single transaction bond, include the entry number and shipment identifiers if required by the filing process.

Step 7: Name the parties exactly

- Principal name must match the importer of record or the entity conducting the bonded activity.

- If there are co-principals (for example, joint operators), list each one with full legal names.

- Surety name must match its registered name. The agent must sign as attorney-in-fact.

Step 8: Add required riders and addenda

- Condition addendum: include the condition text that aligns with your activity.

- Name change or merger rider: file a rider if your legal name changed or you merged with another entity.

- Address change rider: update the bond if your mailing address changes.

- Substitution or termination rider: file if you replace the bond or cancel. Understand that cancellation is prospective and does not cut off liability for past activity.

Step 9: Signatures and authority

- Principal signs. Use the signature block that matches your entity type. Include title for corporate signers.

- Surety’s attorney-in-fact signs. The agent’s power of attorney must be valid on the execution date.

- If filing on paper, include dates and any required seals. If filing electronically, your agent submits through the customs bond system using the power of attorney on file.

Step 10: File the bond and confirm acceptance

- Your agent or broker submits the bond for customs acceptance. For many users, this is electronic.

- Wait for confirmation that customs has accepted the bond. Do not expect release of goods until you have confirmation.

- Keep a copy of the bond, riders, and the power of attorney in your records.

Step 11: Maintain and monitor

- Track your bond sufficiency. If your import volumes or duties increase, you may need a higher continuous bond amount.

- Renew or replace the bond before it expires. Continuous bonds remain in place until canceled, but the surety may require renewal documentation.

- Update riders promptly if your name, address, or corporate status changes.

Step 12: Understand specific entry tie-ins

-

- Importer Security Filing: a continuous importer bond typically covers your ocean security filings. A single transaction may require a separate filing bond if you do not have a continuous bond.

- Temporary importations under bond and similar special programs: confirm that your bond amount covers the special conditions tied to these entries.

- Post-entry actions: your bond covers supplemental duties and compliance requests. Respond to customs notices on time to avoid claims.

Common Mistakes to Avoid

- Using an incorrect legal name for the principal. Make sure it matches the importer of record.

- Setting the penal sum too low. Customs can reject the bond or demand an increase, delaying release.

- Missing condition addenda. Customs will not accept the bond without the correct conditions.

- Assuming cancellation clears past liability. It does not. The bond remains liable for entries during its active period.

- Ignoring power of attorney validity. An expired or missing power of attorney for the surety agent will cause rejection.

- Failing to tie a single transaction bond to the correct entry. This can delay cargo release.

Practical examples

If you import once for a trade show, you might choose a single transaction bond. You coordinate with a surety or broker, set the bond amount to cover the shipment’s exposure, and file the bond with the entry. After the show, when customs liquidates the entry and no claims arise, the bond fulfills its purpose and lapses.

If you import every week, you choose a continuous bond. You size it based on your expected duties, taxes, and fees. You file the bond once and keep it active. Your broker files entries under that bond. If your volumes increase over the year, you review your bond sufficiency and increase the amount if needed.

If you run a container station at a port, you select the custodial bond conditions. You provide your facility details and inventory control plans to customs as part of your operations. The bond covers your receipt, custody, and transfer of bonded goods. You file riders if your facility address changes.

If you claim drawback refunds each month, you post a drawback bond. The bond supports accelerated payments. If customs later determines some portion of your claims was not eligible, it can make a demand under the bond.

If you manage a foreign trade zone, you use the form to post the required bond for zone operations. The bond supports admissions, reporting, and inventory control. You maintain it as long as you run the zone.

Final checks before you submit

- Confirm the activity matches your actual operations.

- Verify names, EIN, and addresses.

- Confirm the penal sum and effective date.

- Confirm the surety and agent authority.

- Attach the correct condition addendum and any necessary riders.

- Keep proof of customs acceptance.

By following these steps, you can complete CBP Form 301 accurately and keep your shipments and operations on track. The bond gives customs confidence that you will meet your obligations. It gives you a faster path to release and a stable framework for ongoing imports and bonded activities.

Legal Terms You Might Encounter

Principal means the party responsible for the bond’s obligations. On this form, you are the principal if you import, act as an importer’s agent, operate a bonded facility, or file security data. Your legal name and identification number must match your official records because the bond ties your liability directly to that identity.

Surety is the company that guarantees your obligations to customs under the bond. The surety steps in if you do not pay duties, taxes, fees, or penalties. On the form, the surety appears by name and code and signs through an attorney-in-fact. Without an authorized surety signature, the bond is not valid.

Obligee is the party protected by the bond. Here, the obligee is the government agency administering customs laws. When you agree to the bond’s conditions, you promise to perform those conditions in favor of the obligee, including paying amounts owed and complying with cargo and entry requirements.

Penal sum is the maximum amount the surety must pay under the bond. You select the penal sum based on your expected activity. For continuous bonds, the amount must be high enough to cover your annual exposure. For single transactions, it must cover that entry. If the penal sum is set too low, you risk rejection or demands to increase coverage.

Continuous bond is a bond that stays in force until terminated. It covers multiple transactions for a defined activity code, such as importing or filing security data. On the form, you indicate continuous coverage, pick an effective date, and ensure the penal sum aligns with your ongoing volume. You do not need a new bond for each entry while it remains active.

Single transaction bond (sometimes called a single-entry bond) covers one entry or one transaction. You use it when you import infrequently or for a special shipment. On the form, you enter the specific transaction details tied to that entry. Once customs clears and the transaction completes, the bond’s obligation narrows to that entry’s liabilities.

Activity code describes what the bond covers. Common activity codes include import entries, security filings, bonded warehouse operations, and carriers. On the form, you must pick the correct code that matches your role. Selecting the wrong activity code can delay clearance, trigger rejections, or leave you uncovered for the activity you actually perform.

Conditions of bond are the promises you make. They include paying duties, redelivering goods on demand, following marking rules, maintaining records, and obeying other requirements. The form incorporates these conditions by reference. Signing means you accept them. If you violate a condition, customs can make a claim against you and the surety.

Power of attorney authorizes someone to act on behalf of another. You may grant your broker authority to sign and file the bond for you. The surety’s attorney-in-fact also signs under a power of attorney to bind the surety company. On the form, you should confirm the signer has valid authority; otherwise, customs can reject the filing.

Rider is an amendment that changes a bond term after issuance. You use riders to update your legal name, address, penal sum, or to add activity coverage. Riders must be signed by both the principal and the surety’s authorized signer. When your business changes, a rider keeps your bond accurate without issuing a brand-new bond.

Cancellation or termination ends bond coverage on a future date. For continuous bonds, either you or the surety can request termination through the required process. On the form, termination terms appear in the bond conditions. Remember that termination does not erase liabilities that arose before the effective termination date.

Bond number is the unique identifier for your bond. Customs and your broker use it to associate entries, filings, and claims with your bond. After the surety issues the bond, you should share the bond number with anyone who files entries or security data on your behalf so it is used correctly on every transmission.

FAQs

Do you need a continuous bond or a single transaction bond?

Choose a continuous bond if you import regularly or have ongoing activities like security filings or bonded facilities. It stays active until you end it and avoids posting a bond for each entry. Choose a single transaction bond if you import infrequently, have a one-off shipment, or the shipment poses special risk and requires higher coverage. If you are unsure, look at your projected total duties, fees, and the number of entries. Frequent importers generally save time and money with a continuous bond.

Do you need a bond if you use a customs broker?

Yes. A broker can file entries and help obtain the bond, but the bond must still cover the principal responsible for the obligations. You remain liable as the importer of record, even if a broker assists. If the broker signs the form for you, confirm they have your power of attorney and that your legal name and identification number appear correctly.

Do you need a bond for low-value shipments or informal entries?

Often, informal entries for low-value shipments may not require a bond. But once you cross certain value thresholds or if your goods are subject to special duties, quotas, or other enforcement, a bond is typically required. If you import regularly, a continuous bond is usually more efficient regardless of shipment values. When in doubt, check the entry type and your activity code to determine coverage needs.

Do you need a separate bond for security filings?

Security filings can require their own coverage if you or your agent file those data elements. A continuous bond can include that activity if structured correctly. If you file security information directly, confirm your bond covers that activity code. If a carrier or another party files on your behalf, ensure the right entity is bonded for that role.

Do you need to increase your bond amount during the year?

You may need to increase your penal sum if your import volume or duties grow. Customs and your surety monitor exposure. If your activity exceeds the coverage, you can receive notices to raise the amount. You can add a rider to increase the penal sum midterm. Do not wait for a stop on entries; adjust proactively when your forecasts climb.

Do you need a new bond after a name change or corporate restructuring?

Name changes, mergers, or tax ID changes require action. If your legal name or identification number changes, you must update the bond through a rider or replace the bond. A simple address change also needs an update. Do not keep filing under an old identity. Mismatches can cause entry delays, bonding gaps, or rejected transmissions.

Do you need original signatures or seals?

Electronic filing is common and accepted. The surety’s attorney-in-fact must have valid authority. If you sign on paper, follow signature and notarization rules that apply to your submission method. Regardless of format, your signature capacity must be clear and supported by internal authority (e.g., officer title or a company resolution if needed).

Do you need to cancel your continuous bond when you stop importing?

Yes, if you stop importing or switch to another structure, you should terminate. Request termination through your surety or filing channel. Keep in mind, terminating does not remove liabilities that arose before termination. Retain records and remain available to address any post-entry issues, including adjustments or penalty notices.

Checklist: Before, During, and After

Before signing

- Confirm your legal name exactly as registered with federal tax authorities.

- Verify your identification number (such as EIN or SSN) is correct.

- Gather your business formation documents and any name change records.

- Decide on continuous or single transaction coverage based on import plans.

- Select the correct activity code for your role and filings.

- Estimate the penal sum using projected duties, fees, and filing exposure.

- Choose an effective date that aligns with upcoming entries or filings.

- Identify your surety and confirm they are authorized to issue bonds.

- If a broker will sign, prepare a power of attorney authorizing them.

- Prepare internal authorization for the person who will sign for you.

- Collect your physical address and mailing address for the bond.

- List any facilities or locations relevant to your activity code.

- Prepare contact information for bond-related notices.

- For single transaction bonds, gather shipment-specific details.

During signing

- Check the principal’s name and identification number for exact matches.

- Verify the address, including suite or unit numbers, is accurate.

- Confirm the activity code covers your intended transactions.

- Review the bond’s conditions and ensure you accept the obligations.

- Verify the penal sum is sufficient for your expected exposure.

- Check the bond type: continuous or single transaction.

- Confirm the effective date and any termination terms.

- Ensure the surety name and code are correct and up to date.

- Verify the surety’s attorney-in-fact signature and authority.

- If using a broker or agent, confirm their authority to sign for you.

- Attach any required riders for name, address, or amount changes.

- Review all dates, signatures, and titles for consistency.

- Retain a copy of the signed bond and any riders for your records.

After signing

- File the bond through electronic channels or with the relevant office.

- For single transaction bonds, file with the entry package as required.

- For continuous bonds, confirm acceptance and activation in the system.

- Share the bond number with your broker and anyone filing on your behalf.

- Update internal procedures so every entry uses the correct bond number.

- Monitor import volume. Increase the penal sum with a rider if needed.

- Amend promptly for name, address, or ownership changes.

- Track termination dates if you plan to cancel the bond.

- Keep copies of the bond, riders, and acceptance confirmations.

- Maintain entry and bond records for the required retention period.

- Set calendar reminders for periodic bond reviews with your team.

Common Mistakes to Avoid

- Picking the wrong activity code. Your bond must match your role. Using the wrong code can cause entry holds, rejected security filings, or uncovered liabilities. Don’t forget to confirm the code covers every activity you perform.

- Underestimating the penal sum. If your import volume grows, your bond can become inadequate. Customs may demand an increase or halt entries until you adjust. Don’t wait for a stop; review monthly and raise the amount with a rider when needed.

- Mismatched legal name or identification number. A small naming error or outdated tax ID can block acceptance and delay clearance. Don’t forget to use the exact legal name and current ID from your official records.

- Missing signature authority or power of attorney. If the signer lacks authority, the bond may be invalid. That can stall entries and force re-filing. Don’t forget to document signer capacity and attach a power of attorney when an agent signs.

- Failing to update after business changes. New addresses, name changes, mergers, or ownership changes require amendments. If you ignore updates, you risk misapplied entries and uncovered activities. Don’t forget to file riders promptly when your business information changes.

What to Do After Filling Out the Form

1. Confirm acceptance. After filing, verify the bond is approved and active. For continuous bonds, check that the effective date and amount display correctly in your filing channel. For single transaction bonds, confirm linkage to the intended entry.

2. Distribute the bond number. Share the bond number with your broker, logistics team, and any third party who files entries or security data for you. Give them your legal name and identification number to prevent mismatches.

3. Align internal systems. Update your enterprise and accounting systems with the bond details. Ensure your entry templates, invoices, and duty estimates reference the correct bond number and settings. Consistency reduces errors at the time of entry.

4. Monitor import activity. Compare monthly duties, fees, and filing volume against your penal sum. If your activity is trending higher, contact your surety to increase the amount through a rider. Act before peak season or large projects.

5. Amend when facts change. File riders when you change your legal name, identification number, address, or ownership structure. If your role changes, update the activity code or obtain additional coverage. Keep the bond aligned with your current operations.

6. Manage renewals and terminations. Continuous bonds do not expire on a fixed date, but they can be terminated. If you plan to stop importing or switch to a different coverage strategy, request termination with a future effective date. Keep the bond active until all open entries and obligations are resolved.

7. Respond to notices promptly. If you receive a notice about insufficient coverage, unpaid amounts, or a required amendment, act quickly. Delays can lead to holds, penalties, or forced bond increases. Keep a designated mailbox and point of contact for bond communications.

8. Keep records. Retain the executed bond, riders, acceptance confirmations, related entry documents, and internal authorizations. Store them securely with your import records for the required retention period. Make them accessible to staff who handle entries and audits.

9. Coordinate with your logistics partners. Confirm your carriers, warehouses, and other service providers understand your bond coverage. Make sure security filings and entries consistently reference your bond number and correct party names.

10. Plan for special transactions. For unusually high-value or complex shipments, assess whether your continuous bond is sufficient. You might need a separate single transaction bond or a temporary increase. Plan early so your coverage is in place before cargo arrives.

11. Establish a change-management routine. Any corporate change can affect your bond. Build a checklist for your legal, finance, and logistics teams to trigger bond updates whenever you change your name, address, tax ID, or ownership.

12. Train your team. Provide quick guides for your staff on when to use the bond, how to reference it on entries, and how to escalate issues. Clear internal steps reduce filing errors and speed up clearance.

Disclaimer: This guide is provided for informational purposes only and is not intended as legal advice. You should consult a legal professional.